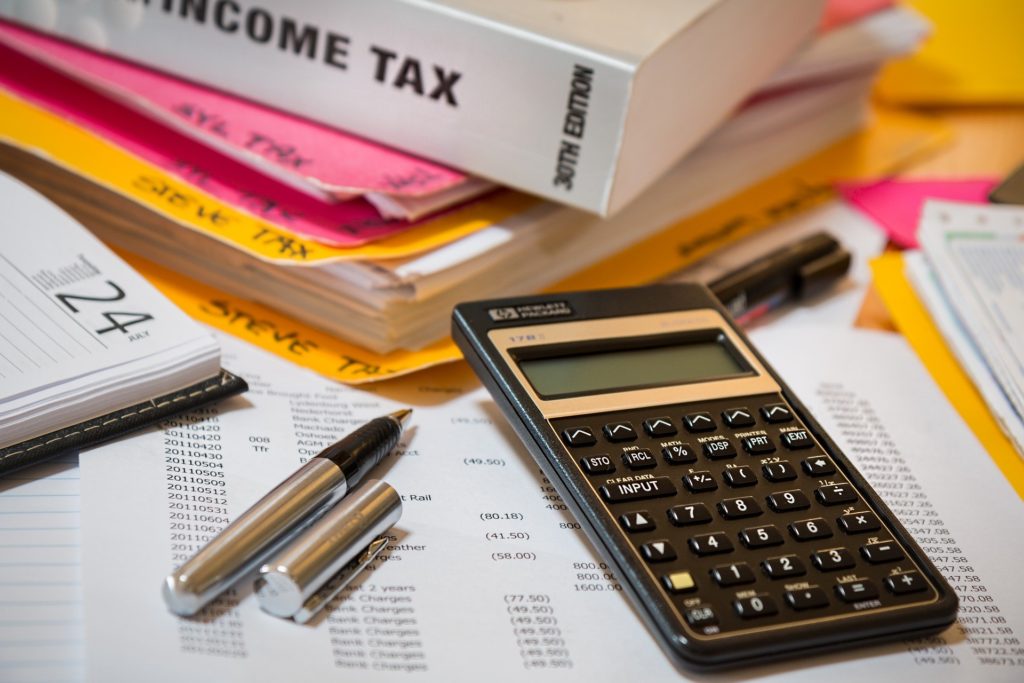

Financial Planning Guide

The way to carrying on with a rich life is assuming responsibility for your money. You don’t must have a six-figure salary or own a business to fabricate riches. You should simply have keen cash sparing propensities and plan for your financial future.

Dissimilar to most cash “specialists” out there, I won’t stay here and instruct you to quit purchasing Espresso at Starbucks or begin cooking rice and chicken for supper consistently. Financial opportunity implies you have power over your choices. For myself, I realize when to spend excessively and I realize where to cut savagely.

On the off chance that you follow the tips and assets that I’ve laid out in this guide, you can bid farewell to money frustration.

Money Planning 101: Basic Things to Sort Out

Financial planning isn’t about penny-squeezing, huge budget spreadsheets, or working 90 hours of the week to make a decent living. It’s tied in with having the correct frameworks set up to construct riches. I would prefer not to invest all my energy considering cash. I need to accomplish the work forthright, put it on autopilot, at that point return to carrying on with my life.

For certain individuals, living rich methods having the option to travel and invest more energy with their family. Others carry on with a rich life by recruiting an individual cook or purchasing originator garments. Yet, before you can get to that point, you have to sift through the accompanying things first:

Cash Mistakes

Staying away from cash slip-ups can spare you a huge number of dollars, if not millions, for an incredible duration. Half of the fight is understanding what not to do with your cash.

- Cash Mistake #1: Debating minutia — Focusing on minor and unimportant financial subtleties without making a move won’t get you rich. Sparing $0.60 purchasing store-brand oat rather than Cheerios won’t have any kind of effect. Rather than bantering about the wellbeing rates or most sultry stocks at the present time, simply set up a no-expense ledger with programmed reserve funds and speculations. At that point permit your cash to develop for 30+ years.

- Cash Mistake #2: Relying on resolution — such a large number of individuals depend on self-control to keep themselves from eating out or purchasing new garments. Regardless of whether you spare $2 every day on espresso by making it at home, That $730 toward the year’s end isn’t huge except if you’ve really set it aside and contributed it.

- Cash Mistake #3: Waiting — Procrastination is executing your cash. Beginning as right on time as conceivable is the best way to financial opportunity. In the event that a 25-year-old contributes $100 every month for a long time at a 8% return rate, their record will be worth $200,061 by the age of 65. On the off chance that their colleague begins contributing $100 every month at age 35 for a long time, their record would be $149,036 at age 65. Despite the fact that the subsequent individual made commitments for a long time longer, they despite everything got done with $50,000 less in light of the fact that they longer to begin.

Automation

One of the principle reasons why individuals neglect to set aside cash is on the grounds that they depend on their future inspiration. Moving cash from financial records to a bank account or venture account requires exertion.

Setting up a computerized individual fund framework for your bills, payments, and investment funds will dispense with those manual assignments and permit you to concentrate on the things that really matter. Automation is so adaptable, so you can set it up to address the issues of your circumstance.

I for one detest point by point budget plans. Having to continually audit all the exchanges, order everything accurately, and survey small budgets for dark classifications makes me insane.

I’d much rather separate everything into a couple of center classes that is easy to follow. That is the thing that we call a Conscious Spending Plan. To set up a cognizant spending plan, you’ll take a gander at the significant zones of your spending:

- Fixed Costs: 50-60% — Things like lease, utilities, vehicle payments, and medical coverage ought to be generally half of your salary.

- Ventures (investments): 10% — Set aside 10% of your pay for things like a Roth IRA and 401(k).

- Reserve funds (savings) 5-10% — This cash can be utilized for an up front installment on a house, get-aways, and unplanned costs.

- Expenses(guilt-free spending) 20-35% — Leave what’s left for things like eating out, beverages, apparel, and going out to see the films.

When you build up your spending suggestions, you can automate your accounts likewise. Here’s a case of what your automation could resemble:

- Second of the month — Part of your compensation goes legitimately into your 401(k) and the rest is immediate store into your financial records.

- Fifth of the month — Automatically move assets from your financial records to an investment account. Naturally move assets from your financial records to your Roth IRA.

- Seventh of the month — Automatically take care of tabs from financial records and credit cards. Consequently cover off charge card tabs from your financial records.

When you mechanize these payments and investment funds, you’ll realize precisely how much cash is left for you to go through every month. That is the place the irreproachable spending comes in. Spend openly until you’ve spent what’s left. You’ve just dealt with your contributing and sparing. Presently you won’t need to mull over purchasing a sandwich for lunch or getting that $5 mug of espresso.

Shrouded Income (Hidden Income)

The vast majority don’t understand that they are discarding “hidden income” every single month. This is the following thing that you have to set everything straight. Taking advantage of concealed salary can be as basic as making a call. These calls can spare you a great many dollars consistently. You simply need to scrutinize your exchange aptitudes on fixed month to month costs:

- Vehicle protection (car insurance) — Instead of picking a vehicle protection once and never taking a gander at it again, get the telephone and arrange your rate. You should simply examine your present plan, check your inclusion alternatives, and shop around with various suppliers.

- Mobile phone — Compare your month to month use (talk, text, information) to different plans offered by different system suppliers. At the point when you call your mobile phone transporter, start by asking what plans can give you a superior worth. On the off chance that that doesn’t work, you can utilize the contenders’ plans as leverage.

- Bank and Credit Card expenses — Yes, you can really arrange charges from banks and credit cards. Getting an overdraft charge deferred or bringing down rate focuses on intrigue payments can spare you thousands after some time. This can assist you with taking care of your obligation quicker also.

When you’re arranging these costs, don’t make it simple for the client assistance delegates to state “no.” Rather than asking, “would you be able to bring down my month to month charge?” express it as “what other plan alternatives do I have?”

Be set up to walk. Much of the time, individuals fear arranging vehicle protection or wireless plans since they would prefer really not to drop the service.

In all actuality, taking steps to drop gives you the best influence. Regardless of whether it implies raising the discussion to a director, your plan won’t really be dropped until you state the last word.

Investing

I know heaps of individuals who are frightened to put cash in the financial exchange. Be that as it may, there is certainly a triumphant recipe to being a fruitful financial specialist after some time. This is apparently the most ideal approach to assemble riches.

Quit concentrating on attempting to purchase the most sizzling stock today and selling it one year from now for greatest profits. Attempting to beat the financial exchange is certainly not a feasible venture procedure.

You ought to likewise overlook the entirety of the media inclusion about an approaching financial emergency or securities exchange breakdown. In the event that you genuinely accept that the market will develop and recoup over the long haul, you should keep contributing during all economic situations.

The three most huge components for effective contributing:

- Start as right on time as could be expected under the circumstances.

- Invest each month.

- Go with the index funds.

Taking out Debt

In the event that you have negative total assets, the idea of putting away or setting aside cash can appear to be unfathomable. So the principal thing you have to do is dispense with your debt for the last time.

There are five stages get out of debt quick:

- Step #1: Figure out how much obligation you have.

- Step #2: Determine what should be taken care of first (in light of financing costs).

- Step #3: Negotiate a lower APR (yearly rate).

- Step #4: Figure out where the cash to pay your obligation will originate from.

- Step #5: Start making a scratch in your obligations.

Like most zones of cash, getting started in paying obligation is the best thing you can do. In any event, paying an extra $20 every month to begin can have a gigantic effect after some time.

Here’s a basic explanation to grandstand the intensity of making bigger payments. Suppose two individuals each have $5,000 in credit obligation at 14% APR.

- Individual A pays $200 every month. It will take those 32 months to pay the obligation, which will bring about $1,313.96 in interest payments over that time.

- Individual B pays $400 every month. It will take them 14 months to pay the obligation, which will cause $436.46 in interest payments.

The subsequent individual spared almost $900 on interest charges by multiplying their regularly scheduled payment payments. Envision how much cash you can spare by on the off chance that you have $10,000 or $20,000+ of obligation just by paying extra every month.

Earn More Money

The best and quickest approach to improving your financial influence is by earning more money. You can budget, plan, and cut costs all you need. Be that as it may, if your pay doesn’t build, you’re way to financial opportunity will consistently be constrained.

There is a breaking point to the amount you can spare, however there is no restriction to the amount you can gain.

These are the three most effortless approaches to get more cash-flow:

- Get a raise.

- Earn money as an afterthought utilizing aptitudes(skills) you as of now have.

- Start another business.

What might you be able to do with an extra $1,000 every month? Shouldn’t something be said about $5,000 or even $10,000+? The best way to discover is by looking for approaches to build your income.

Financial Planning Advisors: Pros and Cons

Loads of individuals feel overpowered with regards to financial planning, which is justifiable. So it’s normal to look for help from a financial advisor. There are a lot of individuals who have had colossal achievement working with a financial planner. Be that as it may, I know other people who didn’t have as much luck.

Financial Advisor Pros:

- You don’t need to gain proficiency with so much stuff yourself.

- Get your cash in the best accounts to save money on taxes.

- Spare time by having an advisor deal with a portfolio for you.

- Make an individual wealth plan for your particular circumstance.

- Can add an additional barrier to your cash, keeping you from settling on an imprudent choice.

Financial Advisor Cons:

- Costs related with employing an advisor.

- Conceivable Conflict of Interest. A few advisors are likewise expedites, getting payoffs on inadequate items that they sell you. Ensure your financial advisor has a trustee obligation to take a shot at your sake.

- Hard to look a privilege financial advisor for you. Like all specialists, it can take some experimentation to discover somebody who’s really acceptable at their specialty.

Wise Tips

Regardless of whether you choose to work with a financial advisor or not are completely up to you. Simply ensure you search around and do your due tirelessness before making a drawn out responsibility. A decent alternative is to search for a few advisors and give them a shot on littler ventures for an hourly charge. That will give you a superior sense before you have them deal with your whole portfolio.

Conclusion

Legitimate financial management is urgent in light of the fact that it permits you to make opportune, very much educated choices because of evolving conditions. Having the plan in any case will assist you with adhering to your objectives. He additionally suggests mechanizing your choices so you don’t need to depend on yourself to continue using sound judgment again and again. At that point, make certain to disregard your plan.

best prescription allergy pills doctor prescribed allergy medication allergy medication primary name

drugs causing nausea and vomiting buy generic avapro 300mg

brand accutane order generic accutane 20mg order isotretinoin 10mg

where to buy sleeping pill how to buy meloset

amoxil 500mg sale cheap amoxil 500mg amoxicillin 250mg canada

buy azithromycin no prescription azithromycin without prescription buy azithromycin 500mg for sale

cheap neurontin 800mg neurontin pills

azipro 500mg us buy generic azipro 500mg azipro 250mg sale

buy furosemide 40mg without prescription order lasix 40mg without prescription

omnacortil pill omnacortil 20mg without prescription purchase omnacortil pills

cheap generic amoxicillin buy generic amoxil order amoxil 500mg generic

doxycycline 200mg us buy monodox generic

purchase ventolin inhaler albuterol inhalator online buy ventolin inhalator for sale online

augmentin 625mg drug order augmentin 375mg for sale

buy synthroid 100mcg without prescription buy levothyroxine no prescription buy synthroid 150mcg without prescription

vardenafil 20mg pills order vardenafil pills

clomiphene 100mg brand clomiphene 100mg cheap buy clomid 50mg generic

buy zanaflex no prescription buy tizanidine pill zanaflex generic

buy deltasone 10mg pill prednisone oral buy prednisone pills for sale

rybelsus 14 mg pills brand semaglutide buy generic semaglutide 14mg

accutane 40mg sale cheap isotretinoin 40mg oral accutane 40mg

cheap semaglutide 14mg buy cheap rybelsus rybelsus uk

order generic albuterol order ventolin 2mg buy albuterol no prescription

buy generic azithromycin over the counter cheap zithromax 250mg azithromycin for sale

order synthroid 100mcg pills purchase levoxyl sale synthroid us

oral omnacortil omnacortil 20mg price buy prednisolone sale

buy serophene pills buy generic clomiphene serophene medication

buy gabapentin 800mg for sale buy neurontin 100mg without prescription gabapentin 100mg oral

buy furosemide 100mg for sale buy furosemide generic furosemide 40mg oral

sildenafil pills 25mg buy viagra 100mg pill sildenafil australia

order generic doxycycline 100mg vibra-tabs over the counter doxycycline 100mg usa

buy semaglutide online rybelsus without prescription semaglutide 14mg price

play for real online casino games free spins no deposit us free poker games

levitra over the counter purchase vardenafil generic levitra cost

order pregabalin 75mg for sale lyrica for sale how to buy pregabalin

buy generic hydroxychloroquine hydroxychloroquine cheap plaquenil 400mg without prescription

triamcinolone 4mg drug triamcinolone drug aristocort 4mg oral

buy cheap generic desloratadine desloratadine over the counter order desloratadine

order cenforce 100mg for sale cenforce 50mg over the counter buy cheap generic cenforce

order loratadine 10mg online cheap purchase claritin online cheap order claritin 10mg sale

chloroquine over the counter chloroquine 250mg brand chloroquine pills

buy dapoxetine 30mg pills purchase priligy online cheap misoprostol price

purchase glycomet order generic glucophage 1000mg buy glucophage 1000mg generic

order lipitor generic atorvastatin 80mg sale oral lipitor 80mg

zovirax cheap buy zovirax cheap zyloprim order

cheap amlodipine 10mg purchase norvasc online cheap purchase norvasc sale

purchase rosuvastatin ezetimibe oral buy ezetimibe generic

buy zestril online cheap zestril pill lisinopril 2.5mg usa

order toradol pills buy gloperba online cheap order colchicine generic

methylprednisolone canada buy methylprednisolone online cheap order depo-medrol online

purchase inderal pills inderal us order clopidogrel pill

order metoclopramide 20mg generic losartan drug generic losartan 25mg

buy esomeprazole pill order esomeprazole 40mg sale topiramate pills

purchase flomax generic celecoxib 100mg us celecoxib 200mg pills

ondansetron 4mg over the counter buy spironolactone no prescription purchase spironolactone for sale

brand sumatriptan 50mg levaquin 250mg tablet purchase levofloxacin pill

simvastatin 20mg oral zocor 20mg ca order valacyclovir sale

cost avodart cheap avodart 0.5mg buy ranitidine 300mg for sale

buy acillin online cheap order acticlate generic buy amoxicillin pill

propecia 5mg pill fluconazole 200mg sale buy diflucan without a prescription

Здравствуйте. С радостью информируем о выходе улучшенного софта БК Олимп! [url=https://best-olimp-app.ru/]Скачать Olimp[/url] доступно для всех! Приложение теперь более удобнее и функциональнее, обеспечивая доступ к широкому спектру ставок на спорт прямо с вашего мобильного устройства. С новейшим обновлением вы имеете расширенные функции управления вашим счетом, обновленный дизайн для более интуитивного пользования, а также улучшенную скорость работы. Присоединяйтесь к удовлетворенным пользователям и совершайте свои ставки с удовольствием и комфортом в любое время и в любом месте. Загрузите последнюю версию приложения букмекерской конторы сегодня и играйте вместе с Олимп!

Восторгаемся возможностью представить новейшее обновление приложения от БК Олимп для Android! Ваше умение и опыт со ставками на спорт теперь станет еще более увлекательным благодаря обновленному интерфейсу и ускоренной работе программы. [url=https://best-olimpbet-apk.ru/]Букмекерская контора Олимп на андроид[/url] доступно сегодня! С последней версией приложения вы получите прямой доступ к разнообразию спортивных событий прямо с вашего мобильного устройства. Ожидайте новые функции для управления счетом, передовой дизайн для интуитивного использования и значительное улучшение скорости приложения. Присоединитесь счастливых клиентов БК Олимп и наслаждайтесь ставкам где угодно и когда угодно. Установите последнюю версию приложения без промедления и начните выигрывать вместе с Олимп!

С энтузиазмом объявляем о дебюте нового мобильного приложения БК Олимп для Android устройств! Этот релиз значительно трансформирует ваше прежнее взаимодействие с ставками, делая его более интуитивным и эффективным. [url=https://skachat-olimp-app.ru/]Скачать приложение конторы Олимп[/url] уже сегодня! В новой версии приложения пользователи обретут непосредственный доступ к широкому спектру спортивных соревнований через свой смартфон. Улучшенное управление аккаунтом, новаторский дизайн для беспрепятственного навигации и повышенная скорость работы приложения – всё это ждет вас. Станьте одним из удовлетворенных пользователей и испытывайте радость от ставок в любом уголке мира и в любой момент. Получите обновление приложения БК Олимп прямо сейчас и начните новый уровень ставок!

С огромной радостью делимся новостью о релизе обновленной версии мобильного приложения от БК Олимп для Android! Это обновление изменит ваш подход к ставкам на спорт, делая процесс более гладким и эффективным. [url=https://olimpbet-apk.ru/]Скачать приложение БК Олимп[/url] и вы получите доступ без труда к огромному выбору спортивных мероприятий, открытых для ставок прямо с вашего мобильного. Усовершенствованные функции управления профилем, интуитивный дизайн для упрощения навигации и ускорение скорости приложения обещают выдающийся опыт. Присоединяйтесь к сообществу энтузиастичных клиентов и наслаждайтесь ставками в любом месте, в любое время. Скачайте последнюю версию приложения БК Олимп уже сейчас и погрузитесь в мир ставок с комфортом и стилем!

Энергично делимся новостью о выпуске новаторской версии приложения для ставок от БК Олимп на Android! Это обновление преобразует ваш подход к ставкам, делая процесс легким и эффективным. Внедрение новейших технологий позволяет предоставить бесперебойный доступ к огромному массиву спортивных мероприятий с вашего мобильного. [url=https://skachat-olimp.ru/]Букмекерская контора Олимп для андроид[/url] и благодаря последним обновлениям, вы насладитесь упрощенным управлением аккаунтом, интуитивно понятным дизайном для легкости использования и значительно ускоренной работой приложения. Становитесь частью сообществу довольных клиентов БК Олимп, наслаждаясь возможностью делать ставки в любом месте и когда угодно. Скачайте актуальную версию приложения уже сейчас и переходите к новым высотам в мире ставок!

Ищете где [url=https://el-gusto.ru/]el-gusto.ru[/url]? Топовые беспроводные наушники в Москве. Реплика оригинальных AirPods с активным шумоподавлением всего за 2490 рублей. Самые надежные гарнитуры по доступным ценам. Быстро доставим по России.

Ищете где [url=https://el-gusto.ru/]купить лучшую реплику Airpods PRO[/url]? Наилучшие беспроводные наушники в Москве. Копия оригинальных AirPods с активным шумоподавлением со скидкой. Только проверенные гарнитуры по доступным ценам. Быстрая доставка по России.

Искали где [url=https://el-gusto.ru/]купить копию наушников Airpods PRO[/url]? Наилучшие беспроводные наушники в Москве и области. Копия оригинальных AirPods с активным шумоподавлением по скидке. Самые качественные гаджеты по приемлимым ценам. Доставим по России.

В поисках где [url=https://el-gusto.ru/]купить копию Аирподс ПРО в Москве[/url]? Наилучшие беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с шумоподавлением по скидке. Надежные гарнитуры по низким ценам. Доставка по России.

Искали где [url=https://el-gusto.ru/]купить копию Аирподс ПРО[/url]? Качественные беспроводные наушники в Москве. Реплика оригинальных AirPods с шумоподавлением по скидке. Надежные гарнитуры по приемлимым ценам. Быстро доставим по России.

Ищете где [url=https://mdou41orel.ru/]купить копию Airpods PRO[/url]? Наилучшие беспроводные наушники в Москве. Реплика оригинальных AirPods с шумоподавлением по скидке. Самые качественные гарнитуры по низким ценам. Доставка по России.

Ищете где [url=https://mdou41orel.ru/]реплика Airpods PRO[/url]? Качественные беспроводные наушники в Москве и области. Реплика оригинальных AirPods с активным шумоподавлением по цене 2490 рублей. Надежные гарнитуры по доступным ценам. Быстрая доставка по России.

Искали где [url=https://mdou41orel.ru/]купить реплику Airpods PRO в Москве[/url]? Лучшие беспроводные наушники в Москве и области. Копия оригинальных AirPods с активным шумоподавлением по скидке. Проверенные гарнитуры по низким ценам. Доставка по России.

Ищете где [url=https://mdou41orel.ru/]реплика Airpods PRO[/url]? Качественные беспроводные наушники в Москве и области. Копия оригинальных AirPods с шумоподавлением по цене 2490 рублей. Проверенные гаджеты по приемлимым ценам. Доставим по России.

В поисках где [url=https://mdou41orel.ru/]купить копию наушников Airpods PRO[/url]? Качественные беспроводные наушники в Москве и области. Реплика оригинальных AirPods с активным шумоподавлением по цене 2490 рублей. Только качественные гаджеты по приемлимым ценам. Доставим по России.

Искали где [url=https://mdou41orel.ru/]купить реплику Airpods PRO[/url]? Качественные беспроводные наушники в Москве и РФ. Реплика оригинальных AirPods с активным шумоподавлением по цене 2490 рублей. Самые надежные гарнитуры по низким ценам. Доставка по России.

Ищете где [url=https://mdou41orel.ru/]купить реплику Аирподс ПРО в Москве[/url]? Качественные беспроводные наушники в Москве и области. Копия оригинальных AirPods с шумоподавлением по скидке. Проверенные гаджеты по доступным ценам. Быстро доставим по России.

В поисках где [url=https://mdou41orel.ru/]копия наушников Airpods PRO[/url]? Лучшие беспроводные наушники в Москве и области. Реплика оригинальных AirPods с активным шумоподавлением всего за 2490 рублей. Проверенные гаджеты по низким ценам. Быстрая доставка по России.

В поисках где [url=https://mdou41orel.ru/]купить реплику наушников Airpods PRO[/url]? Топовые беспроводные наушники в Москве. Реплика оригинальных AirPods с шумоподавлением по цене 2490 рублей. Проверенные гарнитуры по приемлимым ценам. Быстро доставим по России.

Искали где [url=https://mdou41orel.ru/]купить копию наушников Airpods PRO[/url]? Качественные беспроводные наушники в Москве и области. Копия оригинальных AirPods с активным шумоподавлением по скидке. Только проверенные гаджеты по приемлимым ценам. Доставка по России.

Одни проблемы. [url=https://leon.ru/android/]Приложение леон ошибка[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://leon.ru/android/]Почему не работает леон букмекерская контора[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://leon.ru/android/]БК леон не работает[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://leon.ru/android/]Почему не работает приложение леон[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Приложение бк леон вылетает[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Леон букмекерская не работает[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Почему не работает приложение леон[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Леон не работает приложение[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Леон не работает приложение[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Искали где [url=https://el-gusto.ru/]el-gusto.ru[/url]? Качественные беспроводные наушники в Москве и РФ. Реплика оригинальных AirPods с активным шумоподавлением по скидке. Проверенные гарнитуры по доступным ценам. Доставка по России.

Искали где [url=https://el-gusto.ru/]реплика Airpods PRO[/url]? Топовые беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с активным шумоподавлением со скидкой. Только проверенные гарнитуры по приемлимым ценам. Доставим по России.

Искали где [url=https://el-gusto.ru/]реплика наушников Airpods PRO[/url]? Качественные беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с шумоподавлением по скидке. Только проверенные гарнитуры по приемлимым ценам. Быстрая доставка по России.

В поисках где [url=https://el-gusto.ru/]купить реплику Аирподс ПРО[/url]? Топовые беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с шумоподавлением со скидкой. Надежные гаджеты по низким ценам. Доставка по России.

Искали где [url=https://el-gusto.ru/]купить реплику Airpods PRO[/url]? Наилучшие беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с активным шумоподавлением по скидке. Только качественные гарнитуры по доступным ценам. Быстрая доставка по России.

В поисках где [url=https://mdou41orel.ru/]купить реплику Airpods PRO[/url]? Лучшие беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с активным шумоподавлением по скидке. Только проверенные гарнитуры по приемлимым ценам. Доставка по России.

В поисках где [url=https://mdou41orel.ru/]купить реплику Аирподс ПРО в Москве[/url]? Лучшие беспроводные наушники в Москве. Копия оригинальных AirPods с активным шумоподавлением по скидке. Только качественные гарнитуры по доступным ценам. Быстро доставим по России.

В поисках где [url=https://mdou41orel.ru/]mdou41orel.ru[/url]? Топовые беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с шумоподавлением по скидке. Самые надежные гарнитуры по доступным ценам. Доставим по России.

Искали где [url=https://mdou41orel.ru/]https://mdou41orel.ru/[/url]? Топовые беспроводные наушники в Москве и области. Копия оригинальных AirPods с шумоподавлением всего за 2490 рублей. Только проверенные гарнитуры по доступным ценам. Быстро доставим по России.

В поисках где [url=https://el-gusto.ru/]купить копию Аирподс ПРО в Москве[/url]? Качественные беспроводные наушники в Москве и области. Копия оригинальных AirPods с активным шумоподавлением по цене 2490 рублей. Самые качественные гаджеты по низким ценам. Быстро доставим по России.

Искали где [url=https://el-gusto.ru/]реплика наушников Airpods PRO[/url]? Топовые беспроводные наушники в Москве. Копия оригинальных AirPods с активным шумоподавлением по скидке. Проверенные гарнитуры по приемлимым ценам. Доставка по России.

В поисках где [url=https://el-gusto.ru/]купить реплику наушников Airpods PRO[/url]? Топовые беспроводные наушники в Москве и РФ. Реплика оригинальных AirPods с активным шумоподавлением всего за 2490 рублей. Самые качественные гарнитуры по низким ценам. Быстро доставим по России.

В поисках где [url=https://el-gusto.ru/]реплика Airpods PRO[/url]? Наилучшие беспроводные наушники в Москве и РФ. Реплика оригинальных AirPods с шумоподавлением всего за 2490 рублей. Самые надежные гаджеты по доступным ценам. Доставим по России.

В поисках где [url=https://el-gusto.ru/]реплика наушников Airpods PRO[/url]? Качественные беспроводные наушники в Москве и области. Реплика оригинальных AirPods с шумоподавлением всего за 2490 рублей. Самые надежные гарнитуры по низким ценам. Доставка по России.

Искали где [url=https://mdou41orel.ru/]купить реплику Аирподс ПРО в Москве[/url]? Лучшие беспроводные наушники в Москве и РФ. Копия оригинальных AirPods с активным шумоподавлением со скидкой. Только качественные гарнитуры по приемлимым ценам. Быстрая доставка по России.

Искали где [url=https://mdou41orel.ru/]копия Airpods PRO[/url]? Лучшие беспроводные наушники в Москве и области. Копия оригинальных AirPods с шумоподавлением со скидкой. Только проверенные гаджеты по приемлимым ценам. Быстрая доставка по России.

В поисках где [url=https://mdou41orel.ru/]купить реплику Airpods PRO в Москве[/url]? Лучшие беспроводные наушники в Москве. Копия оригинальных AirPods с шумоподавлением по цене 2490 рублей. Самые качественные гарнитуры по доступным ценам. Доставка по России.

Ищете где [url=https://mdou41orel.ru/]копия Airpods PRO[/url]? Топовые беспроводные наушники в Москве. Реплика оригинальных AirPods с активным шумоподавлением по скидке. Проверенные гарнитуры по низким ценам. Быстрая доставка по России.

Одни проблемы. [url=https://leon.ru/android/]Почему не работает приложение леон[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://leon.ru/android/]Приложение леон ошибка[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://leon.ru/android/]Букмекерская контора леон не работает[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://leon.ru/android/]Не работает приложение бк леон[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://leon.ru/android/]Букмекерская контора леон не работает[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Почему не работает бк леон[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Программа бк леон не устанавливается[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Одни проблемы. [url=https://apps.rustore.ru/app/com.leonru.mobile5]Программа бк леон не устанавливается[/url] и с чем связана данная проблема я не знаю. Но лучше поискать другой источник для скачивания данной программы. Тут тратить свое время не советую.

Всем привет! Предлагаем [url=https://do-zarplaty.xyz/]взять займ срочно[/url] в любом городе. Вы можете получить займ без лишних вопросов и документов. Доступные условия займа и моментальное получение рядом с вами. Набирайте нам для уточнения подробной информации, либо оставляйте заявку на сайте.

Всем привет! Предлагаем [url=https://do-zarplaty.xyz/]быстрый займ онлайн[/url] в любом городе. Вы можете получить финансирование без избыточных вопросов и документов. Привлекательные условия займа и моментальное получение в вашем городе. Наберите нам для уточнения подробной информации, или оставляйте заявку на сайте.

Приветствую! Предлагаю [url=https://do-zarplaty.xyz/]взять деньги в долг онлайн в Минске[/url] рядом с вами. Вы можете получить займ без избыточных вопросов и документов. Доступные условия кредитования и моментальное получение рядом с вами. Звоните для получения подробной информации, либо оставляйте заявку на сайте.

Привет! Предлагаем [url=https://do-zarplaty.xyz/]где быстро получить деньги в долг[/url] рядом с вами. Вы можете получить займ без избыточных вопросов и документов. Приятные условия заема и срочное получение в вашем городе. Наберите нам для уточнения подробной информации, или оставляйте заявку на сайте.

Здравствуйте! Появился вопрос про [url=https://dengizaimy.by/]взять деньги в долг срочно[/url]? Предоставляем стабильный источник финансовой помощи. Вы можете получить финансирование в долг без избыточных вопросов и документов? Тогда обратитесь к нам! Мы предоставляем привлекательные условия кредитования, оперативное решение и гарантию конфиденциальности. Не откладывайте свои планы и мечты, воспользуйтесь предложенным предложением прямо сейчас!

Всем привет! Появился вопрос про [url=https://dengizaimy.by/]где можно взять деньги в долг[/url]? Предоставляем безопасный источник финансовой помощи. Вы можете получить финансирование в займ без лишних вопросов и документов? Тогда обратитесь к нам! Мы предоставляем выгодные условия кредитования, быстрое решение и гарантию конфиденциальности. Не откладывайте свои планы и мечты, воспользуйтесь доступным предложением прямо сейчас!

Привет! Появился вопрос про [url=https://dengizaimy.by/]займы онлайн на карту[/url]? Предоставляем безопасный источник финансовой помощи. Вы можете получить средства в займ без избыточных вопросов и документов? Тогда обратитесь к нам! Мы предлагаем высокоприбыльные условия займа, быстрое решение и гарантию конфиденциальности. Не откладывайте свои планы и мечты, воспользуйтесь предложенным предложением прямо сейчас!

Здравствуйте! Появился вопрос про [url=https://dengizaimy.by/]займ от частного лица[/url]? Предлагаем стабильный источник финансовой помощи. Вы можете получить деньги в займ без лишних вопросов и документов? Тогда обратитесь к нам! Мы предлагаем привлекательные условия кредитования, оперативное решение и обеспечение конфиденциальности. Не откладывайте свои планы и мечты, воспользуйтесь доступным предложением прямо сейчас!

Всем привет! Возник вопрос про [url=https://dengizaimy.by/]займем деньги в долг[/url]? Предлагаем надежный источник финансовой помощи. Вы можете получить деньги в займ без излишних вопросов и документов? Тогда обратитесь к нам! Мы предлагаем выгодные условия кредитования, моментальное решение и гарантию конфиденциальности. Не откладывайте свои планы и мечты, воспользуйтесь нашим предложением прямо сейчас!

Здравствуйте! Предлагаю [url=https://do-zarplaty.xyz/]срочно взять деньги[/url] в любое время. Вы можете получить финансирование без избыточных вопросов и документов. Привлекательные условия кредитования и срочное получение в вашем городе. Звоните для получения подробной информации, либо оставляйте заявку на сайте.

Всем привет! Предлагаю [url=https://do-zarplaty.xyz/]займ на карту срочно[/url] круглосуточно. Вы можете получить деньги без лишних вопросов и документов. Выгодные условия займа и моментальное получение рядом с вами. Звоните для уточнения подробной информации, или оставляйте заявку на сайте.

Привет! Предлагаю [url=https://do-zarplaty.xyz/]получить деньги в долг на месяц[/url] в любом городе. Вы можете получить средства без излишних вопросов и документов. Доступные условия кредитования и срочное получение рядом с вами. Наберите нам для уточнения подробной информации, или оставляйте заявку на сайте.

Привет! Предлагаю [url=https://do-zarplaty.xyz/]объявление деньги в долг[/url] в любом городе. Вы можете получить займ без излишних вопросов и документов. Выгодные условия займа и срочное получение в вашем городе. Наберите нам для уточнения подробной информации, или оставляйте заявку на сайте.

Привет! Возник вопрос про [url=https://financedirector.by/]financedirector.by[/url]? Предлагаем надежный источник финансовой помощи. Вы можете получить деньги в долг без избыточных вопросов и документов? Тогда обратитесь к нам! Мы предоставляем выгодные условия кредитования, моментальное решение и обеспечение конфиденциальности. Не откладывайте свои планы и мечты, воспользуйтесь доступным предложением прямо сейчас!

Всем привет! Появился вопрос про [url=https://financedirector.by/]взять деньги срочно на карту[/url]? Предоставляем надежный источник финансовой помощи. Вы можете получить деньги в займ без избыточных вопросов и документов? Тогда обратитесь к нам! Мы предоставляем выгодные условия займа, моментальное решение и обеспечение конфиденциальности. Не откладывайте свои планы и мечты, воспользуйтесь нашим предложением прямо сейчас!

В настоящее время наши дни могут содержать неожиданные расходы и экономические трудности, и в такие моменты каждый ищет помощь. На сайте brokers-group вам помогут без лишних сложностей. В своей роли агента я стремлюсь распространить эту информацию, чтобы помочь людям в сложной ситуации. Наша платформа обеспечивает прозрачные условия и быструю обработку заявок, чтобы каждый мог решить свои денежные проблемы быстро и без лишних хлопот.

В настоящее время наши дни могут содержать неожиданные расходы и экономические трудности, и в такие моменты каждый ищет надежную поддержку. На сайте займ денег вам помогут без избыточной бюрократии. В своей роли представителя я стремлюсь поделиться этими сведениями, чтобы помочь тем, кто столкнулся с временными трудностями. Наша система обеспечивает прозрачные условия и эффективное рассмотрение запросов, чтобы каждый мог разрешить свои финансовые вопросы быстро и без лишних хлопот.

В настоящее время наши дни могут содержать неожиданные расходы и экономические трудности, и в такие моменты каждый ищет помощь. На сайте brokers-group.ru вам помогут без лишних сложностей. В своей роли агента я стремлюсь распространить эту информацию, чтобы помочь людям в сложной ситуации. Наша система обеспечивает прозрачные условия и эффективное рассмотрение запросов, чтобы каждый мог решить свои денежные проблемы быстро и без лишних хлопот.

В настоящее время наши дни могут содержать неожиданные расходы и финансовые вызовы, и в такие моменты каждый ищет помощь. На сайте срочно взять деньги вам помогут без избыточной бюрократии. В своей роли агента я стремлюсь распространить эту информацию, чтобы помочь людям в сложной ситуации. Наша платформа обеспечивает честные условия и быструю обработку заявок, чтобы каждый мог разрешить свои финансовые вопросы быстро и без лишних хлопот.

В наше время многие из нас сталкиваются с непредвиденными расходами и денежными трудностями, и в такие моменты важно иметь доступ к дополнительным средствам. На сайте деньги в кредит вам помогут быстро и удобно. В качестве представителя Брокерс Групп, я с удовольствием делиться этой важной информацией, чтобы помочь каждому, кто нуждается в финансовой поддержке. Наша система гарантирует честные условия и оперативное рассмотрение запросов, чтобы каждый мог решить свои финансовые вопросы быстро и эффективно.

В наше время многие из нас сталкиваются с непредвиденными расходами и денежными трудностями, и в такие моменты важно иметь возможность взять кредит. На сайте dengizaimy.ru вам помогут быстро и удобно. В качестве представителя Брокерс Групп, я рад делиться этой информацией, чтобы помочь людям, кто нуждается в финансовой поддержке. Наша система гарантирует честные условия и оперативное рассмотрение запросов, чтобы каждый мог решить свои финансовые вопросы с минимальными временными затратами.

В наше время многие из нас сталкиваются с внезапными затратами и денежными трудностями, и в такие моменты важно иметь доступ к дополнительным средствам. На сайте взять денег в долг срочно вам помогут с минимальными усилиями. В качестве представителя Брокерс Групп, я рад делиться этой информацией, чтобы помочь людям, кто нуждается в финансовой поддержке. Наша платформа гарантирует честные условия и быструю обработку заявок, чтобы каждый мог разрешить свои денежные проблемы быстро и эффективно.

В наше время многие из нас сталкиваются с внезапными затратами и экономическими вызовами, и в такие моменты важно иметь возможность взять кредит. На сайте получить деньги в долг вам помогут с минимальными усилиями. В качестве представителя Брокерс Групп, я рад делиться этой информацией, чтобы помочь каждому, кто нуждается в финансовой поддержке. Наша система гарантирует честные условия и оперативное рассмотрение запросов, чтобы каждый мог разрешить свои денежные проблемы быстро и эффективно.

В наше время многие из нас сталкиваются с непредвиденными расходами и денежными трудностями, и в такие моменты важно иметь доступ к дополнительным средствам. На сайте взять деньги в долг вам помогут с минимальными усилиями. В качестве официального представителя Брокерс Групп, я с удовольствием делиться этой информацией, чтобы помочь людям, кто нуждается в финансовой поддержке. Наша платформа гарантирует честные условия и оперативное рассмотрение запросов, чтобы каждый мог разрешить свои денежные проблемы с минимальными временными затратами.

В настоящей эпохе финансовые трудности встречаются часто, и каждый из нас может оказаться в ситуации, когда потребуется дополнительная финансовая помощь. На сайте moneybel.ru помогут решить эти проблемы, предоставляя простой и лёгкий метод займа. Мы осознаём, что время играет ключевую роль, поэтому наш процесс обработки заявок максимально быстр и эффективен. В роли представителя Манибел, наша цель – помочь каждому клиенту преодолеть финансовые затруднения, предложив ясные и выгодные условия займа. Доверьтесь нашей компании, и мы поможем вам в решении ваших финансовых проблем.

В настоящей эпохе финансовые трудности не редкость, и каждый из нас может оказаться в ситуации, когда необходима дополнительная финансовая поддержка. На сайте быстрый займ помогут преодолеть эти трудности, принося простой и лёгкий метод получения кредита. Мы осознаём, что времени на решение проблемы не хватает, поэтому мы обрабатываем заявки оперативно и эффективно. В роли представителя Манибел, наша цель – помочь каждому клиенту преодолеть финансовые затруднения, предложив ясные и выгодные условия займа. Доверьтесь нашей компании, и мы поможем вам в решении ваших финансовых проблем.

В настоящей эпохе финансовые сложности не редкость, и каждый человек может оказаться в ситуации, когда потребуется дополнительная финансовая помощь. На сайте МаниБел помогут преодолеть эти трудности, принося простой и удобный способ займа. Мы понимаем, что время играет ключевую роль, поэтому наш процесс обработки заявок максимально быстр и эффективен. В качестве представителя Манибел, мы нацелены на то, чтобы помочь каждому клиенту преодолеть свои денежные трудности, предложив ясные и выгодные условия займа. Доверьтесь нам, и мы решим ваши финансовые проблемы.

В сегодняшнем обществе финансовые трудности не редкость, и каждый человек может оказаться в ситуации, когда потребуется дополнительная финансовая помощь. На сайте займ онлайн помогут решить эти проблемы, принося простой и удобный способ займа. Мы понимаем, что время играет ключевую роль, поэтому наш процесс обработки заявок максимально быстр и эффективен. В качестве представителя Манибел, мы нацелены на то, чтобы помочь каждому клиенту преодолеть свои денежные трудности, предложив ясные и выгодные условия займа. Доверьтесь нашей компании, и мы решим ваши финансовые проблемы.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение [url=https://zaim-minsk.ru/]взять деньги в долг[/url] предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение займы онлайн на карту предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение взять деньги предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение zaim-minsk.ru предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение займ денег предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

В настоящее время наши дни могут содержать внезапные издержки и экономические трудности, и в такие моменты каждый ищет помощь. На сайте получить займ в Минске вам помогут без лишних сложностей. В своей роли агента я стремлюсь поделиться этими сведениями, чтобы помочь людям в сложной ситуации. Наша система обеспечивает честные условия и эффективное рассмотрение запросов, чтобы каждый мог решить свои денежные проблемы оперативно и без лишних затрат времени.

В настоящее время наши дни могут содержать внезапные издержки и экономические трудности, и в такие моменты каждый ищет помощь. На сайте brokers-group.ru вам помогут без избыточной бюрократии. В своей роли представителя я стремлюсь поделиться этими сведениями, чтобы помочь тем, кто столкнулся с временными трудностями. Наша платформа обеспечивает прозрачные условия и быструю обработку заявок, чтобы каждый мог решить свои денежные проблемы быстро и без лишних хлопот.

В настоящее время наши дни могут содержать неожиданные расходы и финансовые вызовы, и в такие моменты каждый ищет помощь. На сайте деньги в долг онлайн вам помогут без избыточной бюрократии. В своей роли агента я стремлюсь распространить эту информацию, чтобы помочь людям в сложной ситуации. Наша система обеспечивает честные условия и эффективное рассмотрение запросов, чтобы каждый мог решить свои денежные проблемы быстро и без лишних хлопот.

В настоящее время наши дни могут содержать внезапные издержки и финансовые вызовы, и в такие моменты каждый ищет надежную поддержку. На сайте взять деньги в долг в Минске вам помогут без избыточной бюрократии. В своей роли представителя я стремлюсь поделиться этими сведениями, чтобы помочь людям в сложной ситуации. Наша платформа обеспечивает прозрачные условия и эффективное рассмотрение запросов, чтобы каждый мог разрешить свои финансовые вопросы быстро и без лишних хлопот.

В настоящее время наши дни могут содержать неожиданные расходы и экономические трудности, и в такие моменты каждый ищет помощь. На сайте получить деньги в долг вам помогут без избыточной бюрократии. В своей роли представителя я стремлюсь распространить эту информацию, чтобы помочь людям в сложной ситуации. Наша платформа обеспечивает честные условия и быструю обработку заявок, чтобы каждый мог разрешить свои финансовые вопросы быстро и без лишних хлопот.

В наше время многие из нас сталкиваются с внезапными затратами и экономическими вызовами, и в такие моменты важно иметь доступ к дополнительным средствам. На сайте деньги в долг в Минске срочно вам помогут с минимальными усилиями. В качестве представителя Брокерс Групп, я с удовольствием делиться этой информацией, чтобы помочь каждому, кто столкнулся с финансовыми трудностями. Наша система гарантирует прозрачные условия и оперативное рассмотрение запросов, чтобы каждый мог разрешить свои денежные проблемы с минимальными временными затратами.

В наше время многие из нас сталкиваются с внезапными затратами и экономическими вызовами, и в такие моменты важно иметь доступ к дополнительным средствам. На сайте dengizaimy.ru вам помогут с минимальными усилиями. В качестве представителя Брокерс Групп, я рад делиться этой важной информацией, чтобы помочь каждому, кто нуждается в финансовой поддержке. Наша система гарантирует честные условия и оперативное рассмотрение запросов, чтобы каждый мог решить свои финансовые вопросы с минимальными временными затратами.

В наше время многие из нас сталкиваются с внезапными затратами и денежными трудностями, и в такие моменты важно иметь возможность взять кредит. На сайте деньги в долг вам помогут с минимальными усилиями. В качестве официального представителя Брокерс Групп, я рад делиться этой информацией, чтобы помочь каждому, кто столкнулся с финансовыми трудностями. Наша система гарантирует честные условия и оперативное рассмотрение запросов, чтобы каждый мог решить свои финансовые вопросы с минимальными временными затратами.

В настоящей эпохе финансовые трудности не редкость, и каждый человек может оказаться в ситуации, когда необходима дополнительная финансовая поддержка. На сайте получить займ помогут преодолеть эти трудности, принося простой и лёгкий метод получения кредита. Мы осознаём, что времени на решение проблемы не хватает, поэтому наш процесс обработки заявок максимально быстр и эффективен. В качестве представителя Манибел, наша цель – помочь каждому клиенту преодолеть финансовые затруднения, предложив ясные и выгодные условия займа. Доверьтесь нашей компании, и мы поможем вам в решении ваших финансовых проблем.

В сегодняшнем обществе финансовые трудности не редкость, и каждый из нас может оказаться в ситуации, когда необходима дополнительная финансовая поддержка. На сайте взять деньги в долг помогут преодолеть эти трудности, предоставляя простой и удобный способ займа. Мы осознаём, что времени на решение проблемы не хватает, поэтому наш процесс обработки заявок максимально быстр и эффективен. В роли представителя Манибел, наша цель – помочь каждому клиенту преодолеть финансовые затруднения, предоставив прозрачные и выгодные условия кредитования. Доверьтесь нашей компании, и мы поможем вам в решении ваших финансовых проблем.

В сегодняшнем обществе финансовые сложности встречаются часто, и каждый из нас может оказаться в ситуации, когда потребуется дополнительная финансовая помощь. На сайте деньги в долг помогут решить эти проблемы, принося простой и лёгкий метод получения кредита. Мы осознаём, что времени на решение проблемы не хватает, поэтому наш процесс обработки заявок максимально быстр и эффективен. В роли представителя Манибел, мы нацелены на то, чтобы помочь каждому клиенту преодолеть свои денежные трудности, предложив ясные и выгодные условия займа. Доверьтесь нам, и мы решим ваши финансовые проблемы.

В сегодняшнем обществе финансовые трудности встречаются часто, и каждый человек может оказаться в ситуации, когда необходима дополнительная финансовая поддержка. На сайте деньги в долг Минск помогут решить эти проблемы, принося простой и лёгкий метод получения кредита. Мы понимаем, что время играет ключевую роль, поэтому наш процесс обработки заявок максимально быстр и эффективен. В роли представителя Манибел, мы нацелены на то, чтобы помочь каждому клиенту преодолеть свои денежные трудности, предоставив прозрачные и выгодные условия кредитования. Доверьтесь нашей компании, и мы поможем вам в решении ваших финансовых проблем.

В настоящей эпохе финансовые трудности не редкость, и каждый из нас может оказаться в ситуации, когда необходима дополнительная финансовая поддержка. На сайте деньги в долг помогут решить эти проблемы, принося простой и удобный способ займа. Мы осознаём, что время играет ключевую роль, поэтому мы обрабатываем заявки оперативно и эффективно. В роли представителя Манибел, наша цель – помочь каждому клиенту преодолеть финансовые затруднения, предоставив прозрачные и выгодные условия кредитования. Доверьтесь нашей компании, и мы поможем вам в решении ваших финансовых проблем.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение деньги в долг предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение займ денег предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

В настоящей экономической обстановке, где неожиданные финансовые обязательства могут возникнуть в любое время, поиск надежного и удобного источника финансовой помощи становится все более критическим. Предложение получить займ предлагает возможность рассчитывать на быстрое и беззаботное получение необходимых средств без лишних трудностей. Мы ценим ваше время и обеспечиваем оперативную обработку всех запросов. В качестве вашего финансового партнера, наша главная задача состоит в том, чтобы помочь вам преодолеть текущие финансовые препятствия, предоставляя ясные и выгодные условия кредитования. Доверьтесь нам в вашем финансовом путешествии, и мы обеспечим вас надежной поддержкой на каждом этапе.

Внимание, любители ставок! БК Олимп представляет с гордостью последнюю версию своего приложения для Android, которое обещает перевернуть ваш мир ставок к лучшему. Мы полностью пересмотрели приложение, чтобы гарантировать несравненный опыт от ставок на спорт. Скачать контору Олимп на андроид и откройте просмотр разнообразных спортивных событий, который стал удобнее благодаря улучшенному интерфейсу и оптимизированной производительности данных. Подключайтесь к нам и наслаждайтесь возможностью делать ставки в любой точке мира, будь то дома или в отпуске. Получите новую версию приложения прямо сейчас и откройте для себя мир ставок с БК Олимп, где выигрыши становятся реальностью!

Внимание, любители ставок! БК Олимп представляет с гордостью последнюю версию своего приложения для Android, которое обещает изменить ваш мир ставок к лучшему. Мы обновили приложение, чтобы гарантировать лучший опыт от ставок на спорт. Скачать БК Олимп на андроид и откройте просмотр разнообразных спортивных событий, который стал удобнее благодаря новому дизайну и оптимизированной производительности данных. Присоединяйтесь к сообществу БК Олимп и пользуйтесь возможностью делать ставки в любой точке мира, будь то дома или в путешествии. Загрузите это обновление приложения без задержек и откройте для себя мир ставок с БК Олимп, где выигрыши становятся реальностью!

Внимание, любители ставок! БК Олимп представляет с гордостью последнюю версию своего приложения для Android, которое обещает изменить ваш мир ставок на радость. Мы обновили приложение, чтобы гарантировать лучший опыт от ставок на спорт. Скачать Olimp bet для андроид и откройте просмотр разнообразных спортивных событий, который стал проще благодаря улучшенному интерфейсу и ускоренной обработке данных. Подключайтесь к нам и наслаждайтесь возможностью делать ставки где угодно, будь то на диване или в отпуске. Получите это обновление приложения без задержек и погрузитесь в мир ставок с БК Олимп, где победы становятся реальностью!

Внимание, любители ставок! БК Олимп представляет с гордостью новейшую версию своего приложения для Android, которое обещает перевернуть ваш мир ставок к лучшему. Мы обновили приложение, чтобы предоставить вам лучший впечатление от ставок на спорт. Букмекерская контора Олимп на андроид и откройте просмотр разнообразных спортивных событий, который стал проще благодаря улучшенному интерфейсу и ускоренной обработке данных. Присоединяйтесь к сообществу БК Олимп и пользуйтесь возможностью делать ставки в любой точке мира, будь то дома или в путешествии. Получите новую версию приложения без задержек и откройте для себя мир ставок с БК Олимп, где выигрыши становятся реальностью!

Вот оно, свежее обновление от БК Олимп для всех поклонников ставок с Android устройствами! Преобразив наше приложение, мы целимся предоставить вам непревзойденный опыт, делая ставки не только удобными, но и захватывающими. Скачать приложение Олимп бет доступное для игроков! С новым дизайном и ускоренной производительностью, доступ к огромному спектру событий стал проще простого. Ощутите радость от оптимизированной работы с аккаунтом и простоты использования, которые делают каждую ставку волнующим моментом. Забудьте о пропущенных возможностях – установите последнее обновление сейчас же и присоединитесь к довольных пользователей, празднующих каждой ставке с БК Олимп, где каждый шанс на победу ценится.

Вот оно, свежее веяние от БК Олимп для всех энтузиастов ставок с Android устройствами! Изменив наше приложение, мы стремимся предоставить вам непревзойденный опыт, делая ставки не только удобными, но и захватывающими. Скачать Olimp bet для андроид доступно для игроков! С новым дизайном и быстрой обработкой данных, доступ к огромному спектру событий стал легким делом. Испытайте радость от оптимизированной работы с аккаунтом и простоты использования, которые делают каждую ставку особым событием. Забудьте о пропущенных возможностях – скачайте последнее обновление сейчас же и вступите в ряды довольных пользователей, радующихся каждой ставке с БК Олимп, где каждый шанс на победу ценится.

Вот оно, свежее обновление от БК Олимп для всех поклонников ставок с Android устройствами! Изменив наше приложение, мы целимся предоставить вам непревзойденный опыт, делая ставки не только простыми, но и захватывающими. Олимп бет на андроид уже сегодня! С новым дизайном и быстрой обработкой данных, доступ к большому разнообразию событий стал легким делом. Испытайте радость от оптимизированной работы с аккаунтом и интуитивной навигации, которые делают каждую ставку волнующим моментом. Не упустите возможностях – скачайте последнее обновление сейчас же и присоединитесь к довольных пользователей, радующихся каждой ставке с БК Олимп, где каждый шанс на победу высоко оценивается.

Вот оно, свежее веяние от БК Олимп для всех энтузиастов ставок с Android устройствами! Преобразив наше приложение, мы стремимся предоставить вам уникальный опыт, делая ставки не только удобными, но и захватывающими. Скачать Олимп бет возможно сегодня! С новым дизайном и быстрой обработкой данных, доступ к большому разнообразию событий стал проще простого. Испытайте радость от улучшенного управления счетом и простоты использования, которые делают каждую ставку волнующим моментом. Не упустите возможностях – скачайте последнее обновление сейчас же и вступите в ряды довольных пользователей, радующихся каждой ставке с БК Олимп, где каждый шанс на победу ценится.

Не пропустите новинку от БК Олимп для Android! Приложение БК Олимп доступное для игроков. Мы пересмотрели наше приложение, чтобы ваш опыт ставок стал ещё удобнее. С новым интерфейсом и ускоренной обработкой данных, вы получите доступ к широкому ассортименту спортивных событий без усилий. Наслаждайтесь простотой управления аккаунтом и лёгкостью использования, делая каждую ставку особым моментом. Загрузите это обновление сегодня и стартуйте побеждать с БК Олимп, где каждая ставка приносит удовольствие!

Не пропустите новинку от БК Олимп для Android! skachat-olimp-apk доступно для всех. Мы пересмотрели наше приложение, чтобы ваш опыт ставок стал ещё лучше. С новым интерфейсом и повышенной скоростью, вы получите доступ к многообразию спортивных событий без усилий. Оцените простотой управления аккаунтом и лёгкостью использования, делая каждую ставку значимым событием. Установите это приложение прямо сейчас и начните побеждать с БК Олимп, где каждая ставка приносит удовольствие!

Не пропустите новинку от БК Олимп для Android! Olimp bet приложение доступно для всех. Мы пересмотрели наше приложение, чтобы ваш опыт ставок стал ещё удобнее. С переработанным дизайном и ускоренной обработкой данных, вы получите доступ к широкому ассортименту спортивных событий легко и просто. Наслаждайтесь удобством ведения счета и интуитивной навигацией, делая каждую ставку особым моментом. Загрузите это приложение прямо сейчас и стартуйте выигрывать с БК Олимп, где каждая ставка приносит удовольствие!

Не пропустите новинку от БК Олимп для Android! Букмекерская контора Олимп на андроид доступно для всех. Мы обновили наше приложение, чтобы ваш опыт ставок стал ещё удобнее. С переработанным дизайном и повышенной скоростью, вы получите доступ к широкому ассортименту спортивных событий легко и просто. Оцените удобством ведения счета и интуитивной навигацией, делая каждую ставку особым моментом. Загрузите это обновление сегодня и стартуйте побеждать с БК Олимп, где каждая ставка приносит удовольствие!

Запуск обновленной версии приложения БК Олимп для Android уже здесь! Модернизировав функционал, мы сделали процесс ставок еще более увлекательным. Скачать приложение Олимп доступно для ставочников. С обновленным дизайном и ускоренной загрузкой данных, доступ к всему спектру спортивных событий станет легкостью. Наслаждайтесь простотой управления счетом и легкой навигацией, превращая каждую ставку в важное событие. Не теряйте времени, скачайте последнюю версию без отлагательств и присоединяйтесь к победителям с БК Олимп, где ставки приносят наслаждение и победы!

Запуск обновленной версии приложения БК Олимп для Android уже здесь! Переосмыслив функционал, мы сделали процесс ставок еще более увлекательным. Приложение букмекера Олимп доступно для ставочников. С обновленным дизайном и быстрой обработкой, доступ к всему спектру спортивных событий станет игрой. Ощутите удобство управления счетом и легкой навигацией, превращая каждую ставку в важное событие. Не теряйте времени, получите последнюю версию прямо сейчас и присоединяйтесь к победителям с БК Олимп, где ставки приносят наслаждение и победы!

Запуск переделанной версии приложения БК Олимп для Android уже здесь! Модернизировав функционал, мы сделали процесс ставок еще более увлекательным. Olimp приложение доступно для ставочников. С обновленным дизайном и быстрой обработкой, доступ к разнообразию спортивных событий станет легкостью. Наслаждайтесь простотой управления счетом и легкой навигацией, превращая каждую ставку в важное событие. Не теряйте времени, получите последнюю версию без отлагательств и присоединяйтесь к удовлетворенным пользователям с БК Олимп, где ставки приносят наслаждение и победы!

Запуск переделанной версии приложения БК Олимп для Android уже здесь! Модернизировав функционал, мы сделали процесс ставок еще более увлекательным. БК Олимп на андроид доступное для игроков. С обновленным дизайном и быстрой обработкой, доступ к всему спектру спортивных событий станет игрой. Наслаждайтесь простотой управления счетом и интуитивно понятной навигацией, превращая каждую ставку в особенный момент. Не задерживайтесь, получите последнюю версию без отлагательств и присоединяйтесь к победителям с БК Олимп, где ставки приносят наслаждение и победы!

Откройте для себя новейшие обновления в приложении БК Олимп для Android! Приложение Olimp доступно для игроков. Мы улучшили наше приложение, чтобы сделать ваше взаимодействие с ставками более приятным. С новым дизайном и быстрой загрузке данных, вы теперь имеете прямой доступ к широкому ассортименту спортивных событий. Научитесь наслаждаться удобство использования своим аккаунтом и легкость управления, превращая каждую вашу ставку в уникальное приключение. Получите приложение сейчас и начните получать удовольствие от побед вместе с БК Олимп, где каждая ставка принесет успех.

Откройте для себя последние новшества в приложении БК Олимп для Android! Олимп на андроид возможно сегодня. Мы улучшили наше приложение, чтобы сделать ваше взаимодействие с ставками более приятным. С новым дизайном и быстрой загрузке данных, вы теперь имеете прямой доступ к широкому ассортименту спортивных событий. Оцените удобство использования своим аккаунтом и интуитивную навигацию, превращая каждую вашу ставку в уникальное приключение. Получите приложение прямо сегодня и начните получать удовольствие от побед вместе с БК Олимп, где каждая ставка несет радость.

Откройте для себя последние новшества в приложении БК Олимп для Android! olimp-apk доступно для игроков. Мы улучшили наше приложение, чтобы сделать ваше взаимодействие с ставками более приятным. Благодаря усовершенствованному интерфейсу и быстрой загрузке данных, вы теперь имеете прямой доступ к широкому ассортименту спортивных событий. Оцените удобство использования своим аккаунтом и интуитивную навигацию, превращая каждую вашу ставку в значимое событие. Загрузите обновление сейчас и начните получать удовольствие от побед вместе с БК Олимп, где каждая ставка несет радость.

Откройте для себя последние новшества в приложении БК Олимп для Android! Приложение Олимп бет на андроид доступно для игроков. Мы улучшили наше приложение, чтобы сделать ваше взаимодействие с ставками удобным. Благодаря усовершенствованному интерфейсу и быстрой загрузке данных, вы теперь имеете прямой доступ к широкому ассортименту спортивных событий. Научитесь наслаждаться удобство использования своим аккаунтом и интуитивную навигацию, превращая каждую вашу ставку в значимое событие. Получите приложение прямо сегодня и начните получать удовольствие от побед вместе с БК Олимп, где каждая ставка несет радость.

Откройте для себя революцию в мире ставок с новейшей версией приложения БК Олимп для Android! Olimp bet на андроид уже сейчас. Мы освежили приложение, обеспечивая неимоверную простоту использования и быстроту загрузки. Теперь разнообразие спортивных событий находится у вас под рукой с новым дизайном и интуитивной навигацией. Прочувствуйте на себе легкость управления счетом и сделайте каждую ставку значительным событием. Установите это обновление немедленно и выходите на новый уровень ставок с БК Олимп, где каждый выбор может принести победу!

Откройте для себя революцию в мире ставок с новейшей версией приложения БК Олимп для Android! Скачать Олимп уже сейчас. Мы полностью переработали приложение, обеспечивая беспрецедентный уровень удобства и быстроту загрузки. Теперь выбор соревнований находится у вас под рукой с улучшенным дизайном и легкой навигацией. Испытайте на себе простоту ведения финансов и сделайте каждую ставку незабываемым моментом. Установите это обновление сегодня и выходите на новый уровень ставок с БК Олимп, где каждый выбор может принести победу!

Откройте для себя революцию в мире ставок с новейшей версией приложения БК Олимп для Android! free-apk-olimp.ru сегодня и сейчас. Мы освежили приложение, обеспечивая неимоверную простоту использования и скорость доступа. Теперь разнообразие спортивных событий находится у вас под рукой с улучшенным дизайном и легкой навигацией. Прочувствуйте на себе простоту ведения финансов и сделайте каждую ставку значительным событием. Загрузите это обновление сегодня и выходите на новый уровень ставок с БК Олимп, где каждый выбор может принести победу!

Познакомьтесь с новейшим обновлением приложения БК Олимп для Android, преобразующим ваш опыт в мире ставок! Приложение Olimp доступны сегодня для каждого. Передовой дизайн и быстрая загрузка данных обеспечивают легкий доступ к широкому ассортименту спортивных событий. Настройте свой аккаунт с непревзойденной легкостью и навигацией, превращая каждую ставку в волнующее приключение. Загрузите прямо сегодня и начните получать удовольствие от ставок на новом уровне с БК Олимп, где каждое событие – это шанс на успех!

Познакомьтесь с новейшим обновлением приложения БК Олимп для Android, изменяющим ваш опыт в мире ставок! Бесплатно скачать Олимп бет на андроид доступны для всех ставочников. Передовой дизайн и ускоренная обработка данных гарантируют легкий доступ к множеству спортивных событий. Настройте свой аккаунт с непревзойденной легкостью и навигацией, превращая каждую ставку в захватывающий опыт. Скачайте прямо сегодня и начните получать удовольствие от ставок на новом уровне с БК Олимп, где каждое событие – это шанс на выигрыш!

Познакомьтесь с свежим обновлением приложения БК Олимп для Android, изменяющим ваш опыт в мире ставок! Скачать apk Olimp bet доступны сегодня для каждого. Передовой дизайн и быстрая загрузка данных гарантируют легкий доступ к широкому ассортименту спортивных событий. Настройте свой аккаунт с уникальной простотой и навигацией, превращая каждую ставку в волнующее приключение. Загрузите прямо сегодня и начните получать удовольствие от ставок на новом уровне с БК Олимп, где каждое событие – это шанс на успех!

Встречайте обновление от БК Олимп для Android, которое полностью преобразит ваш подход к ставкам! С усовершенствованным интерфейсом и оптимизированной работой, вы обретете доступ к бесконечному множеству спортивных мероприятий буквально в несколько касаний. Приложение БК Олимп доступны для всех. Легкое управление аккаунтом и интуитивная навигация сделают процесс ставок удовольствием. Не упустите возможность обновиться уже сегодня и откройте секреты успешных ставок с БК Олимп, где каждый ваш выбор может привести к успеху!

Встречайте обновление от БК Олимп для Android, которое кардинально изменит ваш подход к ставкам! С переделанным интерфейсом и ускоренной работой, вы обретете доступ к бесконечному множеству спортивных мероприятий буквально в несколько касаний. [url=https://olimp-bet-apk.ru/]Скачать Olimp[/url] доступны для желающих. Легкое управление аккаунтом и интуитивная навигация сделают процесс ставок удовольствием. Не упустите возможность обновиться уже сегодня и разгадайте секреты успешных ставок с БК Олимп, где каждый ваш выбор может привести к успеху!

Встречайте новинку от БК Олимп для Android, которое полностью преобразит ваш подход к ставкам! С переделанным интерфейсом и ускоренной работой, вы обретете доступ к огромному количеству спортивных мероприятий буквально в несколько касаний. Олимп бет на андроид доступны для всех. Простое управление аккаунтом и интуитивная навигация сделают процесс ставок наслаждением. Не упустите возможность обновиться уже сегодня и откройте секреты успешных ставок с БК Олимп, где каждый ваш выбор может привести к победе!

Встречайте новинку от БК Олимп для Android, которое полностью преобразит ваш подход к ставкам! С переделанным интерфейсом и ускоренной работой, вы обретете доступ к огромному количеству спортивных мероприятий буквально в несколько касаний. Приложение Olimp доступны для игроков. Простое управление аккаунтом и интуитивная навигация сделают процесс ставок удовольствием. Не упустите возможность перейти на новый уровень уже сегодня и разгадайте секреты успешных ставок с БК Олимп, где каждый ваш выбор может привести к успеху!

Анонсируем выход новой версии мобильного приложения БК Лига Ставок для Android! Этот шаг полностью преобразует ваш досуг с ставками, делая его более понятным и динамичным. Лига ставок апк немедленно! В обновлении вы найдете прямой доступ к огромному ассортименту спортивных мероприятий прямо с вашего смартфона. Улучшенное управление профилем, передовая концепция дизайна для удобной навигации и значительно более высокая скорость работы приложения – всё это создано для вас. Станьте частью довольных пользователей и получайте удовольствие от ставок в любой точке планеты и в любой момент. Скачайте обновление приложения БК Лига Ставок уже сегодня и выходите на новый уровень ставок!

Рады представить выход обновленной мобильного приложения БК Лига Ставок для Android! Этот шаг полностью преобразует ваш досуг с ставками, делая его ещё удобнее и эффективным. Бк лига ставок скачать бесплатно телефон для всех пользователей! В обновлении вы найдете свободу доступа к многообразию спортивных мероприятий из любой точки с помощью вашего устройства. Усовершенствованное управление профилем, инновационная концепция дизайна для удобной навигации и значительно более высокая скорость работы приложения – всё это создано для вас. Присоединяйтесь к числу довольных пользователей и наслаждайтесь возможностями от ставок где только захотите и в любое время. Установите обновление приложения БК Лига Ставок уже сегодня и переходите к новому этапу игры!

Вашему вниманию предлагается эксклюзивное предложение от БК Лига Ставок – фрибет для новых игроков! Это фрибет позволяет вам испытать удачу без риска потери собственных средств, предоставляя новые горизонты для выигрыша с первых же шагов в мире ставок. Фрибет за регистрацию лига ставок для всех новичков после регистрации! С фрибетом от БК Лига Ставок, вы получаете шанс испытать все преимущества ставок без каких-либо финансовых обязательств. Это идеальный старт для тех, кто хочет погрузиться в мир ставок с минимальными рисками. Воспользуйтесь этим предложением и начните своё приключение в БК Лига Ставок с нашим фрибетом. Заберите свой фрибет сейчас же и стартуйте к выигрышам!

Вашему вниманию предлагается эксклюзивное предложение от БК Лига Ставок – фрибет для новых игроков! Это фрибет позволяет вам сделать ставку без риска потери собственных средств, открывая широкие возможности для выигрыша с первых же шагов в мире ставок. Лига ставок фрибет 1000 новым пользователям после регистрации! С фрибетом от БК Лига Ставок, вы имеете возможность испытать все преимущества ставок без каких-либо финансовых обязательств. Это отличный способ начать для тех, кто хочет погрузиться в мир ставок с минимальными рисками. Воспользуйтесь этим предложением и начните своё приключение в БК Лига Ставок с нашим фрибетом. Активируйте ваш фрибет сейчас же и откройте для себя мир ставок без рисков!