Buying your own home is perhaps one of the most important transactions of your life. It can either save or cost you a lot of money. Every little aspect is to be given special attention to ensure this transaction proves out to be an investment that was worth it.

Starting off in this procedure, you first set a target budget that you will bring forward to buy your own house. Now the question is calculating the right amount that you should be capable of paying.

How do you overcome this starter checkpoint? Well, a home affordability calculator is the answer you’re looking for. This article has brought you everything you need to know about figuring out your budget to afford your own house.

What is a Home Affordability Calculator?

Starting with the basics, a home affordability calculator is, as the name suggests, a tool to compare your income and budget for buying a house. To be able to afford a house of a certain price, your income should be of a specific value. It calculates the amount of money you need to be earning in order to bring forth a certain target value for house affordability.

This is the basic definition of a home affordability calculator. This calculation involves several factors. While the majority of your earnings and expenses are stable, there is likely to be an unexpected spike in either expenses or costs every once in a while. But don’t worry.

The general rule of home affordability calculation takes care of that. So, how exactly does it work? Let us take a look at the basic rules of calculating home affordability prices.

How Does it Work?

To calculate the approximate value of a house, you should be able to afford; the house affordability calculator takes certain factors into account. These include your household income, expenditures, monthly debts such as student loans, etc.

As a home buyer, you should be left with enough amount to settle into your new house without worrying about the coming month’s expenses. Your mortgage, of course, plays a major role in this calculation.

The average percentage of your mortgage should take out of your monthly income is around 25%. This comparison is done when your pre-tax monthly income is compared with your monthly liabilities (not household expenses). Let us look into an example. Suppose your monthly mortgage debt is $1,500. Taxes and insurance are included.

Furthermore, your monthly pre-tax income is $4,000. Therefore, your debt-to-income ratio (DTI) would be 1500/4000=0.26 (26%). This calculation almost fits our criteria of a 25% mortgage payment out of the monthly income.

Home Affordability Calculator FHA

Let us suppose a scenario in which your best bet is a conventional loan in a 25% down payment. But if you’re considering a much lower percentage of down payment, then an FHA loan is best for you. A Federal Housing Administration (FHA) loan is a loan that comes from an FHA approved lender.

These loans are designed for the lower-middle class that is less likely to afford a heavy down payment. Moreover, this loan is suitable for people with lower credit scores. If you’re tight on budget, you can borrow up to 90% of a house’s value through an FHA loan.

This will leave you with a down payment of around only 3%. However, to obtain an FHA loan, your credit score should be at least 580. If these criteria cannot be met, then you’ll have to fall a bit shorter with the down payment. An FHA loan is most widely preferred by first time home buyers and the low/middle class.

Home Affordability Calculator VA Loan

If you’ve been involved with the military, a VA loan just might your cup of tea in buying a house. So, what exactly is a VA loan? A Veterans Affairs loan is a mortgage-backed up by the US government for ex-military personnel. A VA loan can do wonders for you since it does not require a down payment at all. However, only licensed US veterans or widowed spouses are eligible to apply for the VA loan.

The VA loan guarantees that the government will repay the debtor’s debt if they fail to make payments. This support takes out the element of risk for lenders lending money to borrowers. The best part of this loan is that no down payment gets into the frame. So, if you’re an army veteran of the US, your home affordability calculation can easily be backed up by the government itself.

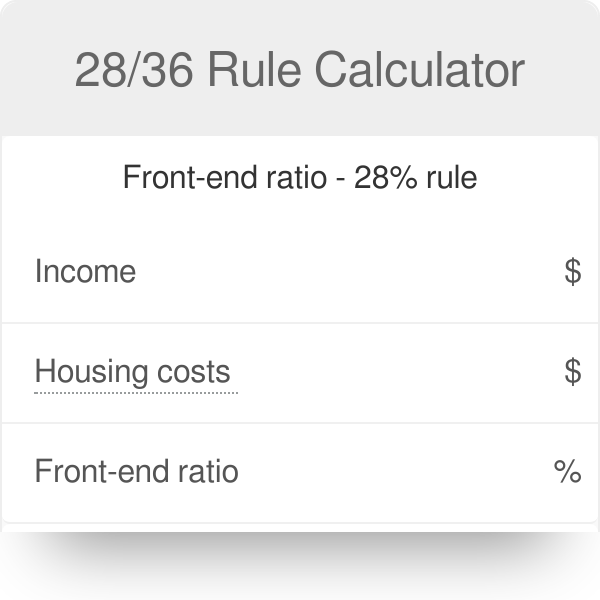

The 28/36 Rule in Home Affordability Calculation

The most common yet best practice in home affordability calculation is the application of the 28/36 rule. This rule determines how much of a mortgage the house buyer is eligible to pay monthly. As we mentioned above, the average mortgage deducted from your monthly income should not go more than 25-30%, 28% to be specific.

Whereas other debts such as student or car loans should not go further than 36% of your pre-tax income. Lenders use the 28/36 rule to analyze this ratio of mortgage and payment.

Some lenders also enable borrowers with higher credit scores to have higher DTI ratios. The 28/36 rule is optimal for calculating your home affordability, but you will still need to bring other factors to this calculation for more accurate results.

Factors You Need to Consider

Home affordability calculation requires some mainstream factors to be taken into account. The following are based on a general perspective. If you have other such aspects that may impact your research in housing affordability, be sure to discuss them with your financial advisor.

-

Monthly Income

Your monthly income is one of the most important factors in the calculation of house affordability. The more stable it is, the more precise the outcome. If your monthly income changes every month, calculate a yearly average to determine a fixed amount. Your income establishes the very base of your housing budget calculation.

-

Cash Reserves

Savings and liquid assets that you own are the second most important factor that plays a part in house affordability calculation. You’ll have to use your savings and reserves to bring forth an accurate overview while using a home affordability calculator.

-

Debts and Liabilities

Your monthly debts, household expenses such as groceries, bills, insurance all fall under the category of liabilities. This amount should be stable too. While unexpected expenses may occur, you should still have a fixed amount set separately for your monthly expenses.

-

Credit Score

Lastly, your credit score is what determines your presentation as a borrower in front of the lender. This score will value the amount of money you’re capable of owing the lender.

Home Loan Calculator Affordability

The amount of loan you will be provided from your lender will require them to ask certain questions. These will be answered through your debt-to-income ratio DTI, your history of paying debts in time, evidence of stable income, down payment, and other relevant finances. If you pass this test, the lender will consider you to be a worthy borrower.

Your credit score will determine your mortgage rate further on, as well as the interest charges. But do remember that lenders do not take your side values into account. Only your current outstanding debts are of interest to them. Other miscellaneous liabilities will not be included in the consideration.

Conclusion

As we mentioned earlier, buying your own home is an important decision. Ensure you’re taking care of legal obligations in this procedure. Furthermore, the best home affordability calculator can easily be accessed through the internet. The affordability calculation depends on the factors of your situation.

Try different calculators and different scenarios to understand the background of this process. We hope all of your questions regarding home affordability were answered clearly in this article. Good luck getting your dream house!

depakote 500 mg uk where can i buy depakote depakote online pharmacy

antivert canada cheapest antivert antivert 25 mg australia

ceftin 500mg usa ceftin otc where can i buy ceftin

cost of diltiazem diltiazem without a doctor prescription diltiazem 90 mg canada

aldactone 100mg coupon cheap aldactone aldactone prices

levaquin cheap order levaquin levaquin 750 mg cost

how to purchase clozapine clozapine 100mg otc cost of clozapine

micardis 20mg united kingdom micardis for sale micardis nz

ceftin purchase buy ceftin ceftin 125mg purchase

tricor 160mg pills order tricor 160mg tricor 160 mg canada

where to buy geodon cheapest geodon how to buy geodon 80 mg

cymbalta 60 mg australia cymbalta 30mg pills cymbalta prices

calcium carbonate 500mg purchase calcium carbonate 500 mg purchase where to buy calcium carbonate

where can i buy cephalexin 500mg cephalexin otc cost of cephalexin

avapro 300mg usa avapro medication how to purchase avapro

clotrimazole without prescription clotrimazole 10g cheap clotrimazole uk

coumadin nz coumadin 2 mg tablets coumadin nz

cheapest price cymbalta 60 mg

buy phenergan over the counter

brand name lipitor cost

trazodone hydrochloride 100mg

best generic finasteride

cafergot price

online rx diflucan

can you buy diflucan over the counter uk

lopressor for afib

generic propecia cheap

provigil online canada

doxycycline pills cost

propranolol tablets

citalopram 40 mg coupon

erectafil canada

online pharmacy reddit

buy nexium over the counter

mexican pharmacy online

vermox india

nolvadex cost

strattera 25 mg price

cafergot tablet

albuterol price in uk

lanoxin buy

buspar over the counter

nexium pharmacy

buy strattera online pharmacy without prescription

suhagra tablet

abilify generic 15 mg

biaxin bronchitis

silagra 100 uk

cafergot

my canadian pharmacy

elimite cream otc

generic cozaar price

diflucan medication canada

cymbalta 40 mg price

suhagra 50mg buy online india

celexa

buy indocin without a prescription

generic amoxil online

combivent 100 mcg 20 mcg

buy yasmin online uk

amitriptyline 100 mg tablet price

phenergan promethazine

xenical tablet price

order lexapro online no prescription

cozaar 100 cost

medicine vermox

provigil online paypal

prescription costs for nexium

elimite coupon

cost of antabuse in australia

flagyl pills over the counter

canada online pharmacy no prescription

propranolol for sale online

indocin 25mg cap

erythromycin price in usa

neurontin 600

vermox 500mg uk

best price cozaar 25mg without a prescription

canadian pharmacy viagra

inderal brand name

phenergan 10mg australia

diflucan usa

where can i get vermox

antabuse uk pharmacy

flagyl antibiotics

nexium 40 price in india

amitriptyline 25 mg tablet price in india

digoxin generic brand name

where to get valtrex prescription

strattera coupon

trustworthy online pharmacy

cheap lipitor online

cozaar 50 mg tabs

amoxil 250 price

cymbalta 40 mg

acyclovir uk prescription

how much is generic cipro

lisinopril tablet

diflucan pill cost

cheap tetracycline

[url=http://sildalis.ink/]sildalis without prescription[/url]

how to get antabuse in canada

pharmacy shop

generic feldene

buy erectafil 5

indocin pill

can i buy indocin

dexamethasone tablets 4mg india

where to get doxycycline

digoxin price in india

where can i purchase diflucan over the counter

phenergan cream 10g

cafergot for sale

amoxil 500mg capsules

robaxin tablets price

seroquel 100mg

160 mg strattera

erythromycin gel

motilium suspension

seroquel 25 mg cost

motilium over the counter canada

zofran otc mexico

generic flagyl cost

dapoxetine buy us

can i buy glucophage over the counter in south africa

canadian pharmacy store

tadacip 20 mg

price for synthroid 150 mcg

us pharmacy no prescription

prescription medication neurontin

where to buy cleocin

buy robaxin australia

motilium 10

albuterol canadian pharmacy

avodart 50 mg

lopressor 50 mg daily

online pharmacy discount code

fildena 50 mg online

robaxin muscle relaxant

can i buy celexa online

canada pharmacy online legit

ventolin purchase

pharmaceuticals online australia

actos united states actos 15mg tablet

robaxin pill

avodart online buy

stromectol xl

tizanidine 6 mg tablets

pharmacy online 365

ivermectin 1%cream

generic super avana

zofran discount

glucophage medicine tablets

motrin 200 mg

cozaar 20 mg price

canadian pharmacy 24h com safe

benicar 5 mg generic

generic brand glucophage

generic propecia online usa

celebrex pharmacy

lisinopril 30mg coupon

bactrim cost

prednisolone over the counter usa

tadalafil 20 mg best price

[url=https://levofloxacina.online/]ebaylevaquin[/url]

where can i get provigil online

disulfiram brand name

what’s the best online pharmacy

tadacip 10 mg price

bupropion sr 100 mg

suhagra online purchase

lisinopril 20 mg no prescription

zanaflex pills

best australian online pharmacy

225 mcg synthroid

avodart uk prescription

lopressor 25 mg

canadianpharmacyworld

avana 50

prazosin 1 mg

celebrex 200 mg cost

erythromycin 500 mg tablet

inderal 40 online

furosemide 20mg tab price

bupropion uk

robaxin 750 mg cost

canadapharmacy24h

lasix vs furosemide

best dapoxetine tablet in india

glucophage xr generic

rate online pharmacies

generic cialis tadalafil 20mg

[url=http://zestoretichydrochlorothiazide.foundation/]cost of hydrochlorothiazide[/url]

levaquin 250mg

amitriptyline pills

bupropion 300 mg cost

seroquel xr and weight gain

ivermectin 5

erythromycin 500 mg coupon

tizanidine best price

dapoxetine 60mg brand name

308186793 benicar

zofran tablet

tamoxifen 10 mg

prazosin 0.5 mg

buy glucophage 500mg online

how to get vermox

glucophage online uk

suhagra buy online

online pharmacy denmark

generic advair canada pharmacy

acyclovir cost uk

140 mg citalopram

buy clonidine canada

where to buy prednisolone 5mg

benicar without prescription

[url=https://lanoxintab.online/]lanoxin 125 mcg tablet[/url]

lipitor 10mg price comparison

average cost of glucophage

price of ivermectin

tizanidine 4mg cost

discount price for glucophage

provigil buy usa

stromectol tablets

uk pharmacy no prescription

[url=http://celecoxib.lol/]price celebrex 200mg[/url]

levaquin 500 tablet

lopid online lopid online pharmacy lopid 300mg no prescription

buy cozaar online

zofran price generic

avana 164

zoloft 50 mg tablet

best value pharmacy

buy cheap dapoxetine uk

where can i buy modafinil usa

chloroquine phosphate 500 mg 7 tablets

propranolol price in india

suhagra 50 mg tablet

buy inderal online uk

accutane pills price in south africa

malegra 50 mg

aurogra 150

0.5 tretinoin cream

abilify pills where to buy

[url=https://celexa.charity/]celexa 1101[/url]

strattera brand name

hq pharmacy online 365

accutane 40 mg daily

phenergan cream 10g

vermox cost

buy celebrex 200mg online

online pharmacy no prescription needed

ivermectin 200 mcg

effexor cost canada

generic finasteride nz

suhagra 200 mg

arimidex tablets price

5 accutane cream

celebrex in mexico

abilify online pharmacy

how much is a medrol 4mg

where to buy xenical

malegra 150

hydrochlorothiazide 25 mg

finpecia online

toradol 60 mg

chloroquine price canada

fildena 100 online

[url=https://erectafil.company/]erectafil 20[/url]

[url=http://levaquin.best/]levaquin 250 tablet[/url]

[url=http://accutane.foundation/]accutane in india price[/url]

triamterene-hctz 37.5-25 mg cp

celebrex price south africa

[url=https://clomidf.online/]clomid 50mg buy uk[/url]

triamterene 37.5 mg hctz 25mg caps

sildalis online

price of levaquin

prescription medication bupropion

celebrex lowest price

arimidex 25 mg price

toradol kidney stones

how much is accutane in canada

zestoretic 10 12.5

malegra 180 on line

cost of albenza medication

how much is advair in canada

effexor xr price

clopidogrel price comparison

150 mg elavil

how much is generic singulair

finasteride uk price

order zofran online without prescription

canada pharmacy 24h

legit canadian pharmacy

lexapro 40 mg

effexor over the counter

malegra dxt

generic robaxin 750

advair medicine

finpecia tablets online

cost of advair in mexico

lexapro 1.25 mg

elimite cost

avana

finpecia 1 mg

ciprofloxacin over the counter canada

cheap elimite

inderal 20 mg price

cymbalta brand coupon

hydrochlorothiazide for sale

erectafil 20 mg price

triamterene brand name

elavil 10 mg

effexor 150 mg cost

buy finpecia

order xenical online

motilium 10mg tablet

where can i get zofran

phenergan australia over the counter

robaxin 75 mg

celexa 60 mg cheap no prescription

dapoxetine price in india

celebrex generic brand

elavil 500 mg

[url=http://diclofenac.directory/]diclofenac brand name canada[/url]

[url=http://albenza.company/]albenza cost generic[/url]

[url=https://xenical.foundation/]xenical orlistat[/url]

[url=https://trental.best/]trental 400 cost[/url]

[url=https://levaquin.gives/]generic for levaquin[/url]

[url=http://atomoxetinestrattera.online/]strattera price canada[/url]

[url=https://prednisonenr.online/]prednisone 40 mg[/url]

[url=https://chloroquine.charity/]buy chloroquine online canada[/url]

[url=https://advairp.com/]advair 115 mcg[/url]

[url=http://toradol.science/]toradol kidney stones[/url]

[url=http://ventolin.party/]albuterol online no prescription[/url]

[url=http://disulfiram.sbs/]antabuse online uk[/url]

[url=https://malegrasildenafil.online/]malegra dxt tablets[/url]

[url=http://celexa.gives/]citalopram 20 mg daily[/url]

[url=http://sildalistabs.com/]buy sildalis 120 mg[/url]

[url=http://diflucani.com/]diflucan 150 mg fluconazole[/url]

[url=https://baclofen.foundation/]baclofen cost india[/url]

[url=https://colchicine2023.com/]colchicine 500 mcg price[/url]

[url=https://erectafil.ink/]buy erectafil 5[/url]

[url=http://retina.africa/]retin a 0.025 cream price in india[/url]

[url=https://lopressor.gives/]price of lopressor[/url]

[url=http://bupropion.party/]bupropion 50 mg[/url]

[url=http://erectafil.ink/]erectafil[/url]

[url=https://triamterene.cyou/]triamterene-hctz 37.5-25 mg capsules[/url]

[url=https://clomid.gives/]buy clomid online[/url]

[url=http://vermoxb.com/]buy vermox online usa[/url]

[url=http://disulfiramtabs.online/]order antabuse online[/url]

[url=https://prednisone.science/]prednisone where to buy uk[/url]

[url=https://baclofen.foundation/]baclofen 25 mg australia[/url]

[url=https://cozaar.charity/]cozaar generic price[/url]

[url=http://piroxicam.gives/]where can i buy feldene gel[/url]

[url=http://malegrasildenafil.online/]buy malegra online[/url]

[url=https://flomax.foundation/]flomax kidney stone[/url]

[url=https://acycloviro.com/]zovirax 200 mg capsule[/url]

[url=http://amoxicillino.com/]order amoxicillin canada[/url]

[url=http://paxil.gives/]paroxetine 40 mg[/url]

[url=http://azithromycin.science/]azithromycin 500mg without prescription[/url]

[url=http://sildalis.download/]sildalis 100mg 20mg[/url]

[url=http://lisinoprilv.com/]lisinopril 30mg coupon[/url]

[url=http://trimox.foundation/]can i buy amoxicillin over the counter in usa[/url]

[url=https://nexium.ink/]generic nexium prescription[/url]

[url=https://lopressor.charity/]lopressor 10 mg[/url]

[url=http://zithromaxc.com/]azithromycin 500 mg generic[/url]

[url=http://piroxicam.gives/]piroxicam cap 20mg[/url]

[url=http://silagrasildenafil.online/]buy silagra india[/url]

[url=https://atenolol.party/]atenolol cost uk[/url]

[url=http://prednisone.africa/]how to get prednisone over the counter[/url]

[url=https://disulfiramtabs.online/]disulfiram uk buy[/url]

[url=https://atarax.foundation/]atarax 25 mg buy[/url]

[url=https://trimox.foundation/]amoxil over the counter[/url]

[url=http://disulfiram.sbs/]antabuse cost us[/url]

[url=http://vermoxb.com/]vermox over the counter uk[/url]

[url=https://diflucan.skin/]buy diflucan otc[/url]

[url=https://tadalafilbv.com/]real cialis for sale[/url]

[url=http://prednisonenr.online/]prednisone 5 mg cheapest[/url]

[url=http://fildena.party/]fildena 50 mg online[/url]

[url=https://inolvadex.online/]tamoxifen cost canada[/url]

[url=https://tamoxifen2023.online/]nolvadex price in india online[/url]

[url=http://colchicine2023.com/]colchicine from mexico[/url]

[url=https://fluconazole.best/]buy diflucan generic[/url]

[url=https://nolvadex.charity/]buy nolvadex online canada[/url]

[url=https://celebrextab.com/]celebrex 200 mg[/url]

[url=https://diflucan.skin/]diflucan pills for sale[/url]

[url=https://silagra.gives/]buy silagra online uk[/url]

[url=https://tadalafil.science/]canada cialis 20mg[/url]

[url=https://erectafil.ink/]erectafil 20 mg price[/url]

[url=https://lopressor.charity/]lopressor 25 mg[/url]

[url=http://celexa.gives/]citalopram 5 mg[/url]

[url=https://amitriptylinepill.online/]amitriptyline in mexico[/url]

[url=http://cozaar.charity/]cozaar 50 mg sale[/url]

[url=https://nolvadextabs.com/]20 mg tamoxifen[/url]

[url=http://permethrinelimite.online/]buy elimite cream online[/url]

[url=http://erectafil.sbs/]buy erectafil 20[/url]

[url=https://finasteridem.com/]can i buy propecia over the counter uk[/url]

[url=https://kamagra.download/]kamagra jelly drug[/url]

[url=http://nolvadex.charity/]buying tamoxifen online[/url]

[url=http://bupropion.party/]best generic bupropion 2019[/url]

[url=https://abilify.charity/]abilify 25 mg[/url]

[url=http://amitriptyline.gives/]12.5 mg elavil[/url]

[url=http://prozac.party/]can you buy prozac online[/url]

[url=https://ampicillina.online/]ampicillin 250 mg tablet[/url]

[url=https://amitriptylinepill.online/]can i buy amitriptyline online[/url]

[url=https://clomid2023.com/]clomid 50 mg for sale[/url]

[url=http://lopressor.gives/]cost of lopressor 50 mg[/url]

[url=https://diclofenac.boutique/]voltaren gel cheap[/url]

[url=http://ampicillina.online/]canadian pharmacy ampicillin[/url]

[url=https://biaxina.online/]biaxin price canada[/url]

[url=https://finasteride.africa/]brand name propecia online[/url]

[url=https://fluconazole.best/]cheap diflucan online[/url]

[url=http://permethrin.party/]elimite 5 cream over the counter[/url]

[url=https://triamterene.cyou/]triamterene hctz 75 50[/url]

[url=https://tamoxifen2023.online/]where to buy nolvadex[/url]

[url=http://zoloft.skin/]cost of zoloft 50 mg[/url]

[url=http://retina.africa/]retin a prescription online[/url]

[url=http://acyclovir.foundation/]zovirax 800 mg[/url]

[url=http://accutanepill.online/]accutane prescription cost uk[/url]

[url=https://hydroxychloroquinepill.online/]plaquenil hydroxychloroquine cost[/url]

[url=https://tenormin.best/]generic for tenormin[/url]

[url=https://albenzaalbendazole.foundation/]albendazole over the counter uk[/url]

[url=http://synthroidb.com/]synthroid rx[/url]

[url=https://prednisone.men/]prednisone pharmacy[/url]

[url=https://diflucanb.com/]diflucan 500[/url]

[url=http://biaxin.cyou/]biaxin medicine[/url]

[url=http://augmentin.download/]amoxicillin price in india[/url]

[url=https://kamagrasildenafil.foundation/]kamagra oral jelly sydney[/url]

[url=https://budesonide.foundation/]budesonide over the counter[/url]

[url=http://zanaflex.gives/]zanaflex tablet[/url]

[url=https://diclofenac.ink/]how much is diclofenac[/url]

[url=http://cytotec.charity/]cytotec sale singapore[/url]

[url=http://flagyl.lol/]flagyl antibiotics[/url]

[url=https://finasteridel.com/]cheap finasteride 5mg[/url]

[url=http://bactrim.party/]bactrim ds 800 160[/url]

[url=http://diflucan.gives/]where to buy diflucan pills[/url]

[url=http://budesonide.foundation/]budesonide canadian pharmacy[/url]

[url=https://flomax.ink/]how to get flomax[/url]

[url=http://tadalafilh.com/]cialis 800mg[/url]

[url=http://diclofenac.ink/]voltaren 1 mg[/url]

[url=https://flagyl.lol/]buy cheap flagyl[/url]

[url=https://dipyridamole.best/]dipyridamole 25 mg tab[/url]

[url=http://piroxicam.cyou/]piroxicam buy online[/url]

[url=https://nexium.gives/]nexium cost australia[/url]

[url=https://trimox.best/]how can you get amoxicillin[/url]

[url=https://chloroquine.foundation/]nivaquine[/url]

[url=http://malegra.charity/]malegra fxt[/url]

[url=https://atomoxetinestrattera.foundation/]strattera pill price[/url]

[url=http://baclofenr.com/]baclofen discount[/url]

[url=https://dexamethasone2023.com/]over the counter dexamethasone cream[/url]

[url=https://provigil.foundation/]buy modafinil india[/url]

[url=https://wellbutrin.foundation/]wellbutrin brand[/url]

[url=http://doxycyclinedx.online/]doxycycline 50[/url]

[url=https://albenza.science/]albendazole tablets price[/url]

[url=https://celecoxib.foundation/]buy celebrex[/url]

[url=https://zanaflex.gives/]tizanidine without prescription[/url]

[url=http://prazosin.charity/]prazosin medication[/url]

[url=http://nexium.charity/]nexium prices usa[/url]

[url=http://tamoxifen2023.com/]nolvadex rx[/url]

[url=http://zestoretic.gives/]zestoretic 10 12.5[/url]

[url=http://baclofenr.com/]buy baclofen online[/url]

[url=http://stromectola.charity/]where to buy stromectol[/url]

budesonide online

robaxin generic south africa

atenolol 100 mg tablet

canada pharmacy happy family store

trental 400 mg online order

diflucan prescription uk

cost of advair 250 50

retin a 0.05 cream price

dexona 8mg tablet

diflucan uk online

[url=https://nexium.gives/]nexium cost[/url]

cost of acyclovir 400 mg

best price nexium online

valacyclovir valtrex

cipro.com

accutane generic

prazosin 5 mg cap

tadacip online india

lisinopril 40 mg price in india

silagra pills

order robaxin online

[url=https://bactrim.party/]buy cheap bactrim[/url]

amoxicillin 500 generic

zithromax 500mg canada

celebrex capsule

cheap benicar

feldene generic

where to buy robaxin

erectafil 20 mg

nolvadex 40mg

online pharmacy cipro

buy robaxin uk

lyrica 500 mg tablet

piroxicam 10 mg

motilium medication

cost of brand name lisinopril

baclofen 10 mg lowest price

Hello! order isotretinoin beneficial web page http://accutanis.top

stratera

buy baclofen online australia

Hi! ed drugs good internet site http://erectiledysfunctionpillsx.online

mexico viagra over the counter

erectafil online

Howdy! purchase ed drugs good site http://erectiledysfunctionpillsx.online

triamterene-hctz 75-50

dipyridamole tablets

baclofen 25 mg tablets

zithromax online pharmacy

diflucan over the counter canada

clomid pills uk

Howdy! purchase ed drugs great internet site http://erectiledysfunctionpillsx.online

buy lasix online usa

Hello! buy ed drugs no rx excellent internet site http://erectiledysfunctionpillsx.online

where to buy prozac

how to purchase over the counter generic robaxin from canada

Hi there! ed drugs cheap great site http://erectiledysfunctionpillsx.online

can you buy phenergan over the counter phenergan gel over the counter phenergan uk

No hassle in buying 100 doxycycline pills from this website.

Hi there! best online pharmacy without prescription beneficial website http://onlinepharmacyxls.com

My insurance doesn’t cover the full cost of Synthroid 50mcg, so I’m looking for a more affordable option.

propeciaoffers.com finasteride tablets propecia prescription uk cost

atenolol 50mg without prescription atenolol tablets atenolol 50 pill

As a representative of a competing pharmacy, I have to say that the price of generic Strattera is a strong selling point.

fluoxetine 30 mg uk buy prozac online uk fluoxetine prices usa

fildena tablets fildena 100 fildena 50 online

I’ve been able to cut down on my ADHD medication thanks to modafinil 50mg.

pharmacy express viagra online canadian pharmacy foreign online pharmacy

Howdy! pharmacy tech online program excellent web site http://onlinepharmacyxls.com

suhagra tablet cheapest suhagra suhagra 25 mg price

Hi there! top online pharmacies beneficial web page http://onlinepharmacyxls.com

The tadalafil pills price is a prime example of pharmaceutical greed.

Cipro 500mg has been associated with rare cases of serious side effects, such as nerve damage or blood vessel rupture.

dexona medicine dexamethasone cream price dexamethasone uk

Patients should be aware of the Doxycycline 40 mg price and how it may impact their health care budget.

how much is tamoxifen tamoxifen no prescription order nolvadex online

Hi! pharmacy technician online good site http://onlinepharmacyxls.com

Hello there! cvs pharmacy job application online good site http://onlinepharmacyxls.com

advair prescription price advair coupon canada advair 100 50 mg

albendazole in india buy albendazole canada albenza albendazole

medication canadian pharmacy medical pharmacy south pharmacy websites

Hello! best online pharmacy no prescription needed beneficial site http://onlinepharmacyxls.com

atarax 25 mg over the counter atarax tablet price atarax tablet price

An Accutane order may require a waiting period before you can start taking the drug.

cytotec 800 mg can you buy misoprostol over the counter cytotec for endometrial biopsy

Hello there! online pharmacies canada great site http://onlinepharmacyxls.com

advair diskus price comparison advair diskus medication advair 115

best price for estrace cream cheap estrace cream generic estrace cream price

Hi there! azithromycin best online pharmacy excellent web site http://onlinepharmacyxls.com

vermox canada where to buy vermox online vermox 500

buy modafinil canada provigil no prescription modafinil uk fast delivery

propecia for sale canada finasteride 1mg no prescription finasterid

Hi there! top rated ed pills very good site https://sildalisxm.online

where can i buy phenergan [url=http://phenergan.ink/]phenergan otc usa[/url] phenergan cost in india

hydrochlorothiazide 150mg hydrochlorothiazide order on line hydrochlorothiazide 50mg tab

big pharmacy online canadian pharmacy prices online pharmacy delivery usa

Allopurinol medication can be taken with or without food.

priligy 30mg buy online super avana tablets priligy online pharmacy

Hi there! ed pills excellent web site https://sildalisxm.online

medrol 4 mg medrol 10mg solu medrol

price of generic advair advair diskus 250 cheap advair 150

suhagra 100 pill suhagra 100 online purchase suhagra tablet price

cymbalta brand name coupon [url=https://duloxetine.cyou/]cymbalta 200 mg[/url] cymbalta 60 mg price canada

atarax for insomnia buy atarax 25mg buy atarax without prescription

kamagra jelly canada cheap kamagra oral jelly 100mg kamagra 50 mg price in india

Hi there! erectile dysfunction medication beneficial website https://sildalisxm.online

After taking doxycycline hyclate 100 mg cap, my symptoms cleared up quickly.

celexa tablet drug citalopram citalopram 4741

Aviator Спрайб

казино Pin-Up

Aviator Spribe гэмблинг

Слоти онлайн у казино Pin Up Casino

Hello! sildalis 100mg good internet site https://sildalisxm.online

albenza 200 mg albenza generic albendazole 200 mg coupon

cost for prozac fluoxetine otc otc prozac

Looking for a reliable source to buy Clomid USA? Look no further!

Howdy! over the counter erectile dysfunction pills excellent web page https://sildalisxm.online

dexamethasone 500 dexamethasone 0.25 mg tablet dexamethasone tablet online

Don’t waste your time searching for modafinil in local stores. Buy modafinil online in USA hassle-free.

erythromycin tablet price erythromycin 500 mg erythromycin over the counter usa

xenical pharmacy buy orlistat online buy xenical from canada

Hello! where buy sildalis great web site https://sildalisxm.online

xenical tablet price buy generic orlistat xenical medicine

buy kamagra oral jelly uk cheap kamagra kamagra soft

Howdy! cheapest ed pills online beneficial website https://sildalisxm.online

I want to purchase allopurinol online because I cannot go to the pharmacy.

Hello! united healthcare online pharmacy good website http://xlonlinepharmacy.online

citalopram 206 citalopram 30 mg pill citalopram canada pharmacy

inderal 20 mg price propranolol buy online propranolol generic

antabuse [url=https://disulfiram.charity/]antabuse medication[/url] antabuse price canada

lipitor canada pharmacy lipitor in uk cheap lipitor generic

finasteride for sale propecia australia propecia canada pharmacy

Hello there! levitra online pharmacy excellent web site http://xlonlinepharmacy.online

Hi! online mexican pharmacy excellent site http://xlonlinepharmacy.online

Stratera has allowed me to be more present and engaged in social situations.

Strattera brand name may be recommended for patients who cannot tolerate stimulant medications or have a history of substance abuse.

finasteride medication price of propecia in canada proscar coupon

I was skeptical about the hype around Modafinil 200, but it really does live up to its reputation.

fildena 150 for sale fildena online fildena 100 usa

generic xenical canada xenical pills where to buy xenical tablets 120mg

budesonide capsule brand name budesonide 1mg budesonide 200 mcg

wellbutrin bupropion wellbutrin 25mg zyban over the counter uk

cheap clopidogrel buy plavix 75 mg uk clopidogrel 75 price

online pharmacy in germany canadian pharmacy viagra 100mg cheapest pharmacy prescription drugs

Hi! how much is ivermectin very good web site https://stromectolxlp.com

Before you buy generic tadalafil online, be sure to compare prices and check for discounts or coupons.

Hello! ivermectin 9 mg good web site https://stromectolrf.online

benicar 20 mg tablet benicar 40 mg coupon price benicar 40 mg

atarax 10mg tablet price atarax usa atarax medicine 25 mg

Hi there! ivermectin 0.5% very good web site https://stromectolrf.online

robaxin 500 mg tablets robaxin australia robaxin 75 mg

citalopram benzodiazepine citalopram nz cost of citalopram in canada

Howdy! cost of ivermectin cream good web site https://stromectolxf.online

Can I get a refund or return on Nolvadex 20mg online if I’m not satisfied?

cymbalta prescription cost where to buy cymbalta cheap cymbalta price comparison

Hi there! ivermectin oral excellent site https://stromectolxf.online

budecort usa budesonide 0.25 mg budesonide 1mg

The convenience of being able to buy Synthroid 75 mcg from home was a huge plus for me.

zoloft 250 mg daily buy zoloft without pres zoloft 60 mg

fildena 100 mg online fildena 25 mg fildena 100 online

Hello there! where to buy ivermectin excellent web page https://stromectolrf.top

Don’t compromise your health by trying to buy cheap doxycycline online.

vermox purchase buy vermox online nz vermox without prescription

Hi there! buy ivermectin pills great internet site https://stromectolxf.online

Hi! purchase stromectol very good web page https://stromectolrf.top

bactrim prices bactrim ordering generic for bactrim

Can I take Clomid medication at any time during my menstrual cycle?

priligy over the counter usa buy priligy online uk dapoxetine pharmacy

plavix cheapest price clopidogrel 600 mg plavix 25

Howdy! ivermectin uk great website https://stromectolxf.online

Always use caution when driving or operating heavy machinery while on Synthroid 1 mg.

silkroad online pharmacy best mail order pharmacy canada online pharmacy no prescription needed

tizanidine 44 tizanidine 4 mg generic tizanidine 12 mg

Hello there! stromectol tablets buy online great website https://stromectolxf.online

tamoxifen 20 mg price uk nolvadex 10mg price in india nolvadex prescription

albendazole uk pharmacy albendazole online canada albendazole 200mg

Howdy! stromectol brand excellent internet site https://stromectolxf.online

cost of propecia in india cheap propecia pills cost of proscar in canada

order albuterol from canada albuterol inhalers for sale albuterol rx coupon

priligy price in india generic priligy 60 mg priligy 60mg uk

Hello there! ivermectin ebay great internet site https://stromectolxf.online

zofran drug zofran 30 tablets zofran generic cost

My doctor said I could switch to generic Synthroid, but I regret doing it.

celebrex 500 celebrex celecoxib best price celebrex 200 mg

bactrim ds bactrim ds medication bactrim forte

flomax online canada [url=http://flomaxp.online/]flomax 5 mg[/url] flomax cost

cymbalta 60 mg buy cymbalta without prescription cymbalta otc

fluoxetine 5 mg capsules prozac prescription buy uk generic fluoxetine

kamagra 100 tablets order kamagra oral jelly kamagra 100

Some people worry about the safety of buying drugs online, but you can buy nolvadex canada safely if you take precautions.

Howdy! ivermectin 3mg for lice very good website https://stromectolrf.online

I saved a lot of money by choosing to buy generic Accutane.

Hi! stromectol price great website https://stromectolxf.online

Hi there! buy ivermectin for humans australia good internet site https://stromectolrf.online

how to get orlistat xenical price in south africa orlistat otc uk

Hello there! stromectol without prescription beneficial site https://stromectolrf.top

Hello! ivermectin 50ml very good website https://stromectolrf.top

estrace 1 mg daily estrace cream ingredients estrace pills

estrace 01 cream coupon cost of estrace cream cheap estrace cream

vermox for sale vermox price in south africa vermox 500mg tablet price

pharmacy best price advair

[url=https://fildena.ink/]fildena 120[/url]

Cipro cheap is just a Google search away.

generic vermox vermox online sale vermox medicine

Your healthcare provider may need to adjust the dosage of lisinopril brand if you have diabetes.

buy neurontin online uk neurontin for sale online buy neurontin online

Is it safe to buy Accutane online pharmacy from a website I’m not familiar with?

buy sildenafil from india

buy fildena 50 mg

vermox over the counter uk vermox australia online vermox usa

[url=http://retina.skin/]retin a 0.05 cream for sale[/url]

levaquin without prescription

nolvadex price uk nolvadex from canada nolvadex tablets

biaxin generic biaxin xl 500mg biaxin 500mg tab

can you buy elimite over the counter elimite cream 5 elimite cost

avodart cost canada avodart uk online buy avodart 0.5 mg

flomax for females flomax generic best price drug flomax

where can i get diclofenac diclofenac 1 diclofenac 4

cost of lipitor in mexico 20 mg lipitor price lipitor cost canada

lexapro prices otc lexapro lexapro mexico

I was hesitant to buy generic Accutane, but it turned out to be a great decision.

discount sildalis sildalis 120 mg buy cheap sildalis

where to buy retin a in canada

fildena 120mg

dipyridamole 100mg

singapore sildalis sildalis online buy sildalis 120 mg

erythromycin antibiotic

dexamethasone tablets cost dexamethasone 0.1 cream dexamethasone tablets uk

cleocin t pads cleocin 2 cream cost of cleocin 100 mg

budesonide 1mg

estrace hair loss estrace 5mg estrace pill cost

atarax usa

dexamethasone 2 mg dexamethasone 4 mg tablet online dexamethasone without prescription

neurontin 400 mg price neurontin tablets uk neurontin mexico

buy vermox in usa

trazodone canada trazodone 125 mg trazodone 6161

amoxil amoxil antibiotics buy amoxil 500 mg online

priligy for sale in usa dapoxetine for sale in australia priligy tablets in india price

amitriptylin online purchase of amitriptyline without a prescriton amitriptyline tabs 25mg

generic advair cost advair diskus 250 mg advair diskus 250 cheap

albendazole sale

buy tamoxifen 20mg uk [url=https://tamoxifen247.online/]tamoxifen online order[/url] tamoxifen canada brand

no rx avana

buy diclofenac gel online uk

cleocin hcl 300 mg

avana canada

augmentin canada

When you [url=http://clomidium.online/]buy Clomid USA[/url] from us, you can be sure you’re getting top-quality products.

A major factor in the Synthroid brand name price is whether or not you have insurance coverage.

cleocin over the counter buy cheap cleocin cleocin 150 mg tablets

I found a great deal to buy provigil online no prescription.

tamoxifen price in canada nolvadex 20mg price nolvadex otc

where to buy dapoxetine in usa

I’ve had to switch to a generic brand because of the synthroid 100 mcg cost.

priligy

how much is trazodone cost trazodone 10mg trazodone 5 mg

buy atarax online canada

Clomid nz can help regulate your menstrual cycle and increase ovulation.

cost augmentin augmentin 625 price uk augmentin cheap

dapoxetine pharmacy

buy vermox canada vermox canada price vermox buy online europe

cleocin 300

retin a 0.05 cream for sale

erythromycin online uk

If you’re looking for an Accutane discount, be sure to check with your insurance provider.

buy malegra 100 mg

Looking to buy cheap Accutane? Look no further!

amoxil 875 amoxil 1g tab generic amoxil online

cytotec online canada purchase cytotec online misoprostol for sale

where can i buy priligy in usa

cleocin t gel cleocin price cleocin 150 mg

cost avodart avodart nz avodart 0.5 mg price

amitriptyline 75 amitriptyline 2102 amitriptyline 10

A Clomid order online can help alleviate the stress and uncertainty of infertility.

fluoxetine 10 mg tablet price fluoxetine tablets 60 mg fluoxetine 20 mg prescription

generic augmentin online

discount sildalis 120mg

sildalis cheap

dapoxetine buy

I never noticed a difference between the lisinopril generic brand and the name brand.

Cheap modafinil can be a lifesaver for people struggling with sleep disorders, such as narcolepsy.

cheap nexium tablets

triamterene 37.5 25 mg

finasteride online finasteride online buy finasteride tablet india

buy baclofen india baclofen 20 mg baclofen cream cost

malegra 120mg

buy valtrex online usa

Buy allopurinol and start feeling better.

Choosing the best metformin brand in India can contribute to better long-term health outcomes.

where to buy fildena 100 fildena 150 mg buy fildena 50mg

benicar in mexico buy generic benicar online brand name benicar cost

cost of benicar 40mg best price for benicar 40 mg benicar generic canada

baclofen uk buy online baclofen baclofen over the counter uk

buy fluoxetine no prescription prozac canada price no prescription fluoxetine

I never thought allopurinol 300 mg tablets could make such a difference.

If anyone has any information about where to buy generic Clomid for sale, please let me know.

sildalis tablets

diclofenac brand name

sildenafil prescription nz

[url=http://yasmin.gives/]buy yasmin pill online australia[/url]

buy vermox australia vermox 200mg price of vermox in usa

cleocin t lotion cleocin 300mg cleocin 2 cream

how much is generic estrace cream cost of estrace cream estrace 0.5

priligy online

flomax diuretic generic noroxin flomax 4 mg capsule

cleocin pill price cleocin price in india cleocin 1

canadian pharmacy sildenafil 100mg

generic prednisone cost prednisone 4 tablets daily 20 mg prednisone

biaxin xl buy biaxin biaxin cost

buy sildenafil usa

retin a cream online pharmacy

prednisone 10mg no prescription prednisone without a prescription prednisone 12 mg

how much is elimite cream elimite medication elimite price

malegra dxt tablets

generic flomax capsules cheapest flomax uk where to buy flomax

At this pharmacy, quality comes first. We don’t sell cheap metaformin.

motrin

where can i buy cleocin [url=http://cleocinrem.online/]cleocin antibiotic[/url] cleocin 100mg cost

budesonide 3 mg cheap budesonide budesonide 80

I highly recommend lisinopril 20mg tablets to anyone struggling with hypertension.

vermox medicine vermox otc canada vermox canada price

In order to increase wakefulness, concentration and alertness, it is recommended to buy Modafinil US.

triamterene-hctz 75-50 mg

valtrex tablet buy valtrex online canada where can i buy valtrex online

purchase diclofenac

avana buy avana online avana 845628057582

amoxicillin 200 mg amoxicillin 10mg amoxicillin 1600 mg

triamterene 75 mg

canadian pharmacy india cialis canada online pharmacy canada rx pharmacy

proscar tablets australia proscar purchase online generic proscar 5mg

estrace pills online

cleocin topical gel cleocin 150 mg capsules cleocin acne

biaxin 500 mg tablet buy biaxin cheap biaxin coupon

dipyridamole medication

amoxil 875 mg tablet amoxil price amoxil discount

ventolin canada

I’ve been taking synthroid 0.75 mcg for years now, and I wouldn’t have it any other way.

augmentin 875 mg price augmentin buy online india buy augmentin online no prescription

buy fildena 100 mg

buy retin-a without prescription

sildalis for sale sildalis india buy cheap sildalis fast shipping

motrin 200 mg

buy vardenafil 40 mg generic vardenafil vardenafil hcl 20mg

legitimate online pharmacy canadian prescription pharmacy american pharmacy

motilium usa motilium 10 mg tablet buy motilium online usa

order cleocin online

diclofenac 500g

buy tamoxifen europe buy tamoxifen usa tamoxifen 20 mg coupon

buy sildalis online

cephalexin price india cephalexin 500 coupon cephalexin 250 prescription

malegra 100 for sale

how much is cleocin 300 mg cleocin topical gel how to order cleocin online

motrin cream

yasmin australia

cleocin liquid 24 cleocin 150 mg cap order cleocin online

cost of dipyridamole

dexamethasone canada dexamethasone discount dexamethasone 4 mg tablet online

ventolin prescription australia

ventolin on line

american online pharmacy tops pharmacy canadian pharmacy viagra

A Synthroid brand name coupon a day keeps the high bills at bay.

buy anafranil canada anafranil for ocd anafranil from india

dapoxetine tablets for sale buy dapoxetine online usa dapoxetine generic cheap

yasmin canada

malegra 25

motrin 12.5

cost of permethrin cream can you buy elimite cream over the counter elimite 5 cream

fluoxetine 20 mg tablet fluoxetine brand fluoxetine for sale

online pharmacy in turkey legitimate online pharmacy usa best online pharmacy no prescription

cleocin 150 cost

avodart 0.5 avodart for sale uk avodart 2.5 mg

order erythromycin online

5 mg zoloft 30 pills

Clomid tablets over the counter can boost fertility by stimulating the release of eggs from the ovaries.

rx tizanidine tizanidine pill tizanidine 2 mg capsule

buy diclofenac gel online india diclofenac united states diclofenac online canadian pharmacy

advair diskus price canada

The Accutane prescription process feels like a never-ending battle.

dexamethasone 20 mg tablet dexamethasone tablets 1.5 mg dexamethasone price south africa

levaquin 500

where to buy estrace cream cheap price estrace tablets estrace oral

vermox in usa vermox price nz vermox uk

amoxil 500 mg cost amoxil cost canada amoxil 800 mg

can i buy proscar over the counter how much is generic propecia where to buy propecia in usa

flomax generic otc

order vermox over the counter

vardenafil price vardenafil 20mg without prescription vardenafil generic 10 mg

priligy canada pharmacy

amoxil 250mg amoxil 1g tab cheap amoxil

ebaylevaquin

buy malegra 200 mg

dexamethasone 10 dexamethasone tablet price dexamethasone 4

Lasix 500 mg tablets should never be shared with others.

proscar prescription uk proscar 1mg tablets generic proscar online

order valtrex online usa

Stay positive and proactive in your search for Synthroid discounts, even if success is not immediate or guaranteed.

sildalis cheap buy sildalis online where to buy sildalis

trazodone 125 mg trazodone 75 mg tab trazodone otc price

trazodone without prescription trazodone hydrochloride trazodone generic price

generic finasteride canada generic finasteride online buy finasteride 1mg india

vardenafil 20 mg vardenafil brand name in india vardenafil no prescription

diclofenac gel in india diclofenac 100 mg capsule diclofenac gel over the counter

rx budesonide

how to get toradol

buy tamoxifen online usa where to buy tamoxifen uk nolvadex for sale cheap

where can i get benicar benicar generic price cheap benicar

prozac 50 mg cost fluoxetine medicine buy cheap prozac

triamterene drug

benicar 5 mg generic benicar 20 5 mg benicar generic

buy motilium online usa buy motilium canada buy motilium 10mg

augmentin price india

cleocin lotion cleocin gel cost cleocin

where to get vermox vermox uk buy online vermox 100

amoxil capsules 500mg price order amoxil online amoxil 500mg cost

tretinoin cream india

plavix generic drug generic plavix price online plavix

triamterene hctz 75 50 mg tab

cheap priligy uk

buy finasteride no prescription how much is finasteride finasteride tablet online

neurontin 200 neurontin 800 neurontin gel

fildena 120 mg

dapoxetine uk cost

estrace india

diclofenac pharmacy

discount nexium prescription

Get lasix on line and save time.

proscar hair loss how to buy proscar online generic proscar cost

estrace cream canadian pharmacy

motrin 100 mg

avana drug

Experience the convenience of Clomid without prescription.

online pharmacy without insurance canadien pharmacies mexican pharmacies online drugs

silagra visa silagra silagra uk

budesonide 400 mg budesonide 3 mg price budesonide 6 mg

malegra 25 mg

Medication affordability programs can help reduce the financial burden of Lyrica cost Australia for patients who need the medication.

purchase erythromycin 500mg canada erythromycin tablet erythromycin tablets 500mg price

levaquin drug

The metformin pharmacy price is an important consideration, but it should not be the only factor when selecting a diabetes medication.

diclofenac brand name uk

how much is zoloft generic tablet

Clomid citrate has been a lifesaver for me in my fertility journey.

celebrex medication online

best place to purchase cialis cialis no prescription cialis 40 mg price

motilium mexico motilium canada over the counter motilium pills

tamoxifen uk online tamoxifen brand name canada purchase tamoxifen

neurontin medication neurontin 300 mg cost neurontin 600mg

ventolin pharmacy australia

zoloft 500mg

cost of azithromycin 250 mg in india

amoxicillin 500mg capsule price in india amoxicillin 500 buy amoxicillin online

fildena 100 online india buy fildena 50mg fildena 50

Where to buy modafinil online without getting scammed, anyone know?

advair diskus 550

The cheapest price for lisinopril may be found abroad, but be aware of laws and regulations surrounding importation.

avodart generic avodart 0.55 mg avodart price

avodart for sale avodart for sale online avodart price uk

tamoxifen 10 mg online where can i buy tamoxifen tamoxifen tablets for sale

100mg baclofen baclofen buying baclofen online

Howdy! buy valtrex pills online great site http://valtrexrp.online

The metformin 500 for sale I purchased here has been a game-changer for my health.

avana singapore avana cream avana usa

how much is valtrex canada

buy vermox 500mg vermox canada pharmacy where can i buy vermox over the counter

atenolol 12.5 mg daily prescription atenolol 50 mg atenolol 50 mg cost

cleocin 100mg

erythromycin 500mg buy online where to get erythromycin 250 mg erythromycin tablets

Online pharmacy synthroid can be a convenient way to refill your thyroid medication.

estrace cream cost

amoxil 500 mg price price for amoxil amoxil 500 cost

neurontin for sale online buying neurontin without a prescription neurontin 300 mg cost

buy vermox over the counter

3000mg prednisone

Don’t put your health at risk by buying Lasix online from sketchy websites.

priligy online order

where can i buy vermox over the counter order vermox online where to buy vermox online

motrin capsules

cleocin vaginal ovules

discount sildalis canadian pharmacy sildalis cheap sildalis

In some cases, the Lyrica cost Australia is so high that patients are unable to purchase the full amount prescribed.

cleocin 150 mg capsules

amoxicillin 500 price

levaquin drug

generic avodart from india avodart nz prescription drug avodart

finasteride where can i buy order generic finasteride finasteride how to get

vermox otc

amoxicillin 3107

buy finasteride finasteride 5 mg daily finasteride online pharmacy india

where to buy prednisone without a prescription

estrace 1mg

cephalexin tablets for sale keflex antibiotics cephalexin 500mg buy

ventolin tablets uk albuterol 021 ventolin online australia

where to buy motilium motilium australia motilium price singapore

finasteride online 1mg finasteride where can i buy finasteride 1 mg

can you buy retin a with out prescription

fildena in india fildena 150 mg fildena 25

diclofenac 100 mg capsule

cleocin 2 cream over the counter cleocin topical for acne cleocin hcl used treat

cleocin pill price cleocin 300 mg cost cleocin gel online

[url=https://priligy.pics/]priligy price[/url]

dipyridamole tablets

elimite generic permethrin cost elimite otc

motilium online uk buy no prescription motilium motilium online pharmacy

valtrex 3000 mg

Why do I need a prescription when all I want is to order clomid over the counter?

Howdy! buy valacyclovir pills good web site http://valtrexrp.online

dexamethasone 2.5 mg dexamethasone 0 5 mg dexamethasone 500mcg

clopidogrel buy online clopidogrel coupon can i buy plavix over the counter

celebrex brand name price

cleocin coupon

200 mg celebrex cost

diclofenac 75 mg cost

avodart uk price

best nexium

buy sildalis

sildalis online sildalis cheap buy sildalis 120 mg

Don’t knock the Clomid generic brand until you’ve tried it!

zofran pharmacy zofran tablet price where can i get zofran over the counter

baclofen comparison baclofen 60 mg baclofen

Attempting to acquire modafinil without prescription is not worth the legal consequences.

dapoxetine 60 mg

vardenafil hcl 20mg tab vardenafil brand name in india vardenafil online uk

robaxin 750mg robaxin 800 mg robaxin 500mg generic

buy estrace no prescription

I’m desperately searching for where to get Clomid.

tamoxifen cost india tamoxifen 20 brand name tamoxifen cost nz

best online pharmacy no prescription pharmacy wholesalers canada reputable indian online pharmacy

Lyrica 75 mg capsules are commonly used to treat neuropathic pain.

buy dapoxetine 60mg

priligy pharmacy

canadian pharmacy viagra 50 mg trusted canadian pharmacy online pharmacy pain relief

tamoxifen cost canada tamoxifen tablets brand name buy tamoxifen online usa

celebrex generic over the counter

priligy tablets

how much is erythromycin cream

tretinoin tablets 10mg

flomax generic alternative flomax brand name flomax inhaler

yasmin medicine price in india

tamoxifen 20 mg tamoxifen 5 mg tamoxifen buy online

acyclovir 400mg tablets

buy vermox online uk

Cipro over the counter is not a substitute for regular check-ups and preventative healthcare.

advair diskus discount

buy cheap cleocin

advair diskus canada pharmacy

Allopurinol 209 was a waste of money, it did nothing for my gout.

amoxil 1g amoxil 500mg amoxil 500 cost

dapoxetine india dapoxetine 100 mg priligy dapoxetine

zoloft 200 mg daily

buy zyban bupropion 189 bupropion 50 mg

buy motilium motilium over the counter singapore motilium pills

cleocin 300

cheap prednisone online

albuterol 0063 albuterol sulfate albuterol canadian pharmacy

zoloft 200 mg cost zoloft pill 100 mg zoloft

Howdy! valtrex cheap great site http://valtrexrp.site

proscar 5mg price in usa proscar 1mg online generic proscar cost

erythromycin 500mg cost

generic neurontin 600 mg neurontin 300mg neurontin tablets 100mg

dapoxetine no prescription

cost of tretinoin 0.05

rx budesonide

cost of yasmin pill in australia

dapoxetine pills in india order dapoxetine dapoxetine 30 mg tablet price

vermox 100mg tablets vermox canada vermox buy online europe

I couldn’t imagine getting by without Provigil 100 mg.

order amitriptyline buy amitriptyline tablets buy amitriptyline uk

priligy price in india online

cheap viagra online canadian pharmacy canadian pharmacy online ship to usa online pharmacy

buy avodart avodart 0.5 mg generic where to buy avodart online

baclofen online without prescription baclofen 10 mg tab baclofen 4097

finasteride 0.1 finasteride cheap finasteride 0.5

ventolin over the counter

proscar coupon buy generic proscar proscar pharmacy

cipla cialis price comparison cialis sublingual cialis

motrin sale

The convenience factor of synthroid.com is unbeatable.

amoxicillin 500mg price in india

proscar cost in us can i buy proscar over the counter buy proscar 1mg

dapoxetine pills for sale buy dapoxetine 30mg dapoxetine 60

ivermectin 15 mg stromectol price in india cost of ivermectin medicine

diclofenac tablets in india diclofenac 75 mg pill diclofenac over the counter in europe

order tamoxifen arimidex tamoxifen tamoxifen price in usa

buy amoxil online australia order amoxil amoxil 250 mg

where can i get prednisone

It’s important to understand the potential risks and benefits before deciding to [url=https://accutan.online/]buy Accutane 20mg[/url].

I had a bad reaction to ciprofloxacin hcl.

celebrex 200 mg for sale

[url=http://retina.skin/]where to buy retin a over the counter[/url]

silagra 100 online silagra 100 buy silagra online

lexapro rx lexapro 10 mg tablet lexapro 100mg

can you buy amoxicillin over the counter in mexico

medication cleocin

[url=http://vermox.party/]vermox buy online uk[/url]

avodart drug avodart generic equivalent avodart cheap

buy atarax

motrin 400mg

buy avana

nexium 20 mg tablet

dapoxetine buy canada

I tried to buy generic Synthroid but the website kept redirecting me to the brand name version.

Hello there! buy valtrex cheap good web page http://valtrexrp.site

cleocin 300 mg capsules cleocin medication cleocin for acne

acyclovir pill

retin a moisturizer

amoxicillin 320 mg

amoxil 500 pill amoxil price in usa amoxil

amoxil amoxicillin purchase amoxil generic amoxil

priligy prescription usa

cleocin tablet cleocin vaginal ovules cleocin cream price in india

albendazole prescription

fildena buy order fildena online fildena 100 online

antibiotic cephalexin buy cephalexin mexico cephalexin medicine

price for diclofenac gel

amoxil 400 mg amoxil amoxil without a prescription

brazilian pharmacy online canada drug pharmacy which online pharmacy is the best

order brand name cialis online buy cialis online cheap uk cialis daily online

erythromycin generic 250 mg tablets price

flomax otc uk [url=https://aflomax.com/]flomax no prescription[/url] flomax kidney stone

medicine prednisone 20mg tablets order prednisone without prescription prednisone corticosteroids

how can i get flomax without a prescription flomax for prostatitis flomax 8828

price of advair diskus

clonidine tab 0.1 mg

avodart soft capsules 0.5mg

The lack of transparency from Clomid UK was concerning.

albendazole price in india

where to purchase azithromycin

lexapro wellbutrin lexapro 5 mg lexapro 10 mg cost

yasmin price south africa

cleocin gel generic

The cost-effectiveness of clomid buy online India should be balanced with ensuring the quality and genuineness of the product.

amoxicillin 500mg online uk [url=http://amoxicillin.science/]amoxicillin buy online us[/url] amoxicillin price australia

best dapoxetine tablet in india buy dapoxetine 60mg dapoxetine india

buy ventolin australia

buy cleocin gel online

flomax 0.4 mg in india flomax canadian pharmacy flomax uk cost

cephalexin 400 mg cephalexin tablet price cephalexin buy canada

zoloft 50mg cost

vermox 500 mg tablet vermox australia online vermox online

buy fildena 150 online

phenergan 25 cost medicine phenergan buy phenergan online australia

motrin 300 tablets

priligy tablets for sale

vermox canada cost

avana 200 mg

10 mg baclofen pill buy baclofen 10 mg baclofen 15

Wondering where to buy Clomid in Canada? Look no further!

zofran online prescription how much is zofran order zofran

ampicillin 250 mg tablet

azithromycin buy without prescription

baclofen tablets brand name buy baclofen from india buy generic baclofen

You won’t regret buying Clomid UK.

zoloft generic 100mg

vermox canada pharmacy vermox canada pharmacy vermox cost

buy generic priligy online

order sildenafil

Where to buy modafinil online without getting scammed, anyone know?

buy fildena 150 online fildena india fildena 100 mg for sale

valtrex pills where to buy

0.01 retin a gel

I always take Cipro Flagyl with a light meal to avoid any digestive issues.

ampicillin 250 mg tablet

augmentin 875 cost augmentin online buy buy cheap augmentin

fluoxetin fluoxetine cost australia fluoxetine10mg

diclofenac otc gel

When it comes to managing your ovulation, you can order Clomid online from reliable sources.

how to get flomax rx flomax for urinary retention where can i buy flomax over the counter

albuterol buying albuterol with no prescription albuterol medicine india

cheap finasteride finasteride tablet price finasteride otc

875 mg amoxicillin tablets

can you buy tamoxifen over the counter tamoxifen 20 mg tablet price in india cost of tamoxifen tablets

diclofenac tablets over the counter

amoxicillin pharmacy discount

medication amoxicillin 500mg

levaquin 500 mg

priligy 30

buy zoloft 100mg

buy vermox online nz vermox tablets australia vermox cost

elimite cream generic where to buy elimite where to buy elimite cream

flomax nasal congestion

I don’t know what I’d do without Provigil over the counter – probably sleep all day.

erythromycin estolate

proscar coupon generic for proscar proscar for women

buy amitriptyline 10mg online uk buy amitriptyline 50 mg amitriptyline 25 mg tablet price

where to buy vermox online vermox mebendazole buy vermox online nz

sildalis 120 mg order usa pharmacy where to buy sildalis sildalis

Always follow dosage instructions carefully when making a Clomid buy.

malegra 150

cleocin coupon cleocin hcl 150 mg generic for cleocin

flomax 400 mcg

The availability of Lisinopril without prescription is a growing concern.

over the counter tretinoin

trazodone hydrochloride 100 mg trazodone 20 mg trazodone drug prices

dipyridamole tablets cost

I’m so happy that the Clomid cost UK is not a hinderance to my fertility journey anymore.

how much is benicar generic benicar prices benicar generic cost

I only trust buying Clomid for sale from reputable sources.

purchase amoxicillin online uk amoxicillin 1000 where to buy amoxicillin over the counter

how much is vermox vermox 100mg price vermox pharmacy

Our pharmacy’s customer service is second to none when it comes to where to buy Clomid tablets.

atarax 25

Online clomid is the only option left for me to have a child.

cephalexin 219 cephalexin 250 mg tab how much is cephalexin

cost of atarax 25mg

10 mg baclofen baclofen 25 mg baclofen pharmacy

toradol iv

200mg trazodone 125 mg trazodone discount trazodone

buy stromectol ivermectin for humans ivermectin otc

Do not compromise on quality and safety while trying to buy cheap allopurinol.

purchase medrol medrol 16g buying medrol online

canadian pharmacy no prescription pharmaceuticals online australia canadian pharmacy no prescription

buy generic levaquin

how to buy valtrex in korea

Hello! buy valtrex no prescription good website http://valtrexrp.online

canadian pharmacies compare drugstore com online pharmacy prescription drugs rxpharmacycoupons

where can you buy motilium motilium prescription motilium price australia

1000 amoxicillin

acyclovir 400 mg tablet cost

plavix 75 [url=http://plavixclopidogrel.online/]medicine plavix 75[/url] generic plavix 75 mg

buy vermox uk

erythromycin medicine price

where can i buy prednisone

[url=https://avodart.foundation/]avodart generic equivalent[/url]

buy zoloft 100mg buy zoloft without a prescription can you buy zoloft in mexico

cheap combivent buy ventolin on line albuterol 0.063

Save money on Metformin by shopping with Metformin Buy Canada – it’s that simple!

colchicine acute gout colchicine 6 mg tablet colchicine over the counter australia

buy dexamethasone australia dexamethasone usa dexamethasone 2 mg price

retin a cream prescription cost

purchase cytotec buy misoprostol 200 mcg misoprostol otc usa

Where can I buy allopurinol? I ain’t tryna waste time

flomax sale online

Be sure to store Clomid citrate correctly in order to maintain its effectiveness.

where to buy avodart

buy dapoxetine in india

[url=https://nexium.foundation/]nexium 40 mg price singapore[/url]

cymbalta price online cymbalta otc cymbalta generic usa

levaquin pill

baclofen buy online canada baclofen tablet price generic baclofen buy online

buy generic propecia finpecia online india propecia buy canada

dapoxetine online india dapoxetine prescription order dapoxetine

In rare cases, ciprofloxacin 500mg may cause serious side effects, such as tendonitis or nerve damage.

sildalis cheap

buy plavix online plavix 40 mg plavix 75 mg tablet price in india

motrin capsules

I will never forget to purchase allopurinol again.

budesonide 3mg capsules coupon

amoxil 500 mg brand amoxil 925 amoxil price

amoxil 800 mg generic amoxil amoxil capsule 500mg

prednisone 5mg tablets [url=https://prednisonenr.com/]can i buy prednisone over the counter[/url] prednisone price south africa

plavix rx generic plavix in us plavix 70 mg

amitriptyline uk pharmacy price of amitriptyline amitriptyline tab 100mg

cost for valtrex

atarax 50 mg

albuterol 0.021 generic albuterol inhaler how to buy albuterol online without a prescription

buy diclofenac tablets uk

cephalexin 500mg tablet cost [url=https://cephalexin.science/]cephalexin buy[/url] medication cephalexin 500 mg

Hi! valtrex cheap beneficial web site http://valtrexrp.site

dapoxetine 60

zoloft 125

sildalis 120 mg

What are the potential risks of learning how to buy metformin online?

motilium 10mg tablets medicine motilium 10mg order motilium online

biaxin 500mg biaxin 2500 capsule biaxin price canada

The cost of Synthroid 100mcg feels like a scam.

Patients with renal impairment should avoid taking metformin ER.

tretinoin cream purchase

If I can’t afford a prescription, is it legal to buy clomid over the counter?

bactrim prices bactrim 500 mg tablet bactrim 960 mg

Are Clomid pills effective for fertility treatment?

where can i get erythromycin

buy generic finasteride finasteride over the counter propecia for sale south africa

buy priligy online australia

best generic zoloft brand

buy atarax

clonidine rx

finasteride 1mg generic price finasteride pills for sale where can i buy finasteride

dexamethasone sale dexamethasone 0.5 mg price for dexamethasone

order elimite online elimite otc elimite online

erythromycin cream over the counter uk

generic sildalis

cleocin 75 mg cleocin t pads cleocin t solution

avana canada avana 77064 avana australia

motilium tablet cost motilium 10mg motilium cost

vermox buy online uk

can you buy trazodone in mexico trazodone cheap trazodone prescription cost

levaquin 750 mg

vermox cost canada buy vermox online nz where to get vermox

albendazole price in usa

[url=https://vermox.party/]vermox online pharmacy[/url]

fildena online pharmacy fildena 100 online india fildena 100 online india

vermox 500 vermox drug can i buy vermox over the counter uk

avodart prices canada

Yo, my doctor prescribed me Synthroid medicine for my thyroid problem.

yasmin rizvi

estrace estrogen cream

price of tamoxifen tamoxifen cost nz buy tamoxifen aus

plavix brand name plavix generic pill plavix without prescription

The metformin medicine price is impacting the quality of care for people with diabetes.

canadian pharmacy cialis buy cialis australia where can you buy cialis

levaquin 750mg

clonidine 2 mg

tamoxifen generic brand name tamoxifen 20mg price in india tamoxifen 5 mg

where can i buy toradol

cleocin medicine generic for cleocin cleocin for sinus infection

cost of 5mg tadalafil buy tadalafil no prescription canadian pharmacy cialis brand

generic lexapro 20 mg cost cipralex coupons 20 mg lexapro

Howdy! purchase valacyclovir great site http://valtrexrp.site

I need to buy Clomid no prescription required as soon as possible – can anyone help?

sildalis in india

buy tizanidine no prescription tizanidine 44 tizanidine 10mg price

neurontin 600 mg capsule neurontin 200 neurontin 202

buy albuterol uk proventil albuterol albuterol 0.83 mg

cost of levaquin

toradol pills

water pill triamterene hctz

retin a 1%

10mg prednisone

triamterene 37.25mg

Metformin 100 mg may cause gastrointestinal side effects like diarrhea and nausea.

malegra for sale

prednisone price in usa purchase prednisone for dogs online without a prescription buy prednisone online canada without prescription

I’m willing to take a chance and buy Synthroid from Canada if it means I can afford my medication.

fluoxetine for sale sale no prescription how can i get fluoxetine fluoxetine buy usa

fluoxetine for sale fluoxetine 10 mg canada fluoxetine 10 mg caps

albendazole 200 mg price

dapoxetine generic uk dapoxetine 120 mg dapoxetine 60mg price in india

Lisinopril 5 is a medication that you can take for the long term without any major concerns.

If you’re on a tight budget like me, metformin from India can be a lifesaver.

online pharmacy discount code top mail order pharmacies canadian pharmacy antibiotics

albuterol inhaler albuterol 63 mg albuterol online uk

What’s the best way to make the most of my Synthroid 125 mcg coupon?

Modafinil 100 mg tablet price may fluctuate due to factors such as supply and demand.

buy nexium from canada

I’ve been taking lisinopril 5 mg for a few months now and my blood pressure is stable.

retin a medication

It shouldn’t be this hard to buy Clomid without prescription when it’s proven effective.

acyclovir cream price usa

sildalis 120 mg order canadian pharmacy singapore sildalis sildalis canada

cleocin price cleocin liquid cleocin liquid

how to get nexium cheap

prednisone 5mg price prednisone buy without prescription prednisone 5mg pack

Have you tried searching online for “how to get metformin“?

I have had no success with Lisinopril 40 mg tablets and I don’t recommend them.

vermox over the counter usa

cost of prednisone

can you buy flomax over the counter

purchase amitriptyline amitriptyline online 300 mg amitriptyline

My doctor recommended lisinopril metoprolol but it didn’t control my blood pressure.

usa pharmacy online best rx pharmacy online legitimate online pharmacy

prednisone tablets 2.5 mg canadian pharmacy 5 mg prednisone no rx prednisone 7.5 mg daily

vermox tablets vermox 500mg price order vermox uk

diclofenac 5 0 mg diclofenac brand name uk buy diclofenac 75mg

medrol 16mg how much is medrol medrol tablet 16 mg

cost of dipyridamole

Clomid for men can help improve both physical and emotional symptoms of low testosterone levels.

price of augmentin in india augmentin 125 buy cheap augmentin online

silagra 50 mg silagra 100 mg sale silagra canada

amoxicillin medicine amoxicillin 500mg pill amoxicillin 100 mg coupon

discount sildalis

dapoxetine buy online india

1000 amoxicillin

priligy over the counter

purchase trazodone online trazodone drug trazodone hydrochloride 100mg

cleocin vaginal ovules cleocin suppositories cleocin pill

flomax liquid 12 mg flomax prescription drug flomax

prednisone buying

vermox tablets price

where can i buy dapoxetine in singapore dapoxetine tablets in india dapoxetine pills for sale

fildena buy fildena canada fildena price

buy avodart online no rx

azithromycin online no prescription usa

10 mg prednisone daily

tamoxifen 200 mg tamoxifen buy usa cost of tamoxifen 20mg tablets

The Lisinopril 5 mg tablet was simple to order online and arrived quickly.

[url=https://azitromycin.com/]azithromycin prescription canada[/url]

can you buy amoxicillin over the counter nz

amoxicillin 825

buy prednisone online from canada

motilium suspension motilium tablets over the counter purchase motilium

I’ve recommended this website to several friends who were also searching for cheap Provigil Canada.

avodart prescription uk

buy amitriptyline uk amitriptyline 500mg amitriptyline 5 cream

avana australia [url=https://avana.best/]3131 avana[/url] avana 100

I was skeptical at first, but this [url=http://modafinil.africa/]modafinil coupon[/url] really worked.

amoxil capsule price generic amoxil 500 mg amoxil 1g

augmentin 875 125 mg tablet

How does OTC metformin affect blood sugar levels?

albendazole

where to get vermox vermox vermox without prescription

retin a 0.1 cream mexico

Lyrica 500 mg has become a lifeline for me.

valtrex generic purchase

plavix prescription plavix generic pill cost of plavix 75 mg

amoxil 500 mg amoxil antibiotic amoxil 250 mg tablets

baclofen 10 mg tablet price in india baclofen 5 mg tablet price how can i get baclofen

cleocin 00009766701 cleocin vaginal cream buy cleocin

medicine vermox vermox canada where can i buy vermox in uk

avana canada

clonidine uk cost

generic zoloft no prescription zoloft mexico zoloft 15 mg

cost of estrace cream without insurance

Cipro XR 500 should not be taken if you have a known allergy to any of its ingredients.

biaxin clarithromycin biaxin for ear infection buy biaxin online

baclofen tablet baclofen 10mg tab cost medicine baclofen 10 mg

elimite cream for sale where to buy elimite cream over the counter elimite cream price in india

amoxicillin tablet